Financing Construction Equipment in Africa: 7 Proven Options

How to finance construction equipment in Africa is no longer a tactical decision. It is a strategic lever that determines contractor survival, scalability, and competitiveness in a capital-intensive industry. Across the continent, construction equipment financing in Africa has evolved into a multi-layered ecosystem combining bank lending, leasing markets, asset-backed structures, and institutional capital.

Africa’s infrastructure financing demand ranges from $130 to $170 billion annually, with a persistent funding gap of up to $108 billion, according to the African Development Bank. This gap directly affects contractors, particularly in their ability to access the heavy machinery required for project execution.

Technical Snapshot:

- Equipment financing rates (commercial banks): 12%–25%.

- Leasing market growth (emerging markets): 15–20% annually.

- Equipment ROI threshold: a 3–5 year payback period.

- Infrastructure contribution potential: +2% GDP growth annually (AfDB).

This guide delivers a deep, industry-level breakdown of how to finance construction equipment in Africa, including a step-by-step execution framework, 7 proven financing options, and capital strategy insights used by leading contractors.

Introduction to How to Finance Construction Equipment in Africa

Africa’s construction sector is entering a decisive expansion phase. Governments across Sub-Saharan Africa are accelerating investments in transport corridors, energy infrastructure, housing, and industrial zones. Private capital is also entering the sector, targeting high-growth urban centres.

However, the operational bottleneck remains unchanged: access to heavy construction equipment.

The cost of acquiring machinery such as excavators, motor graders, cranes, and articulated dump trucks typically ranges from $80,000 to over $500,000 per unit, depending on specifications and origin. For contractors managing multiple projects, this capital requirement becomes exponential.

In the current market, understanding how to finance construction equipment in Africa has become a critical requirement for survival rather than an optional luxury. The ability to secure capital directly dictates a contractor’s project mobilisation speed and their overall bidding capacity for large-scale government tenders. Beyond simple acquisition, strategic financing protects profit margins and ensures long-term cash flow stability, allowing firms to scale without exhausting their liquid reserves.

This article provides a comprehensive deep dive into the structure of construction equipment financing in Africa, highlighting the pivotal role that heavy equipment loans play in enabling project execution. We provide a detailed, step-by-step framework for navigating the application process, along with a curated list of the best financing options currently available on the continent. By exploring real-world strategies for financing machinery, this guide serves as a roadmap for leveraging asset finance to drive infrastructure growth.

Understanding Construction Equipment Financing in Africa

To effectively finance construction equipment in Africa, contractors must move beyond surface-level definitions and understand the full financial architecture that underpins the sector. This includes financing structures, capital sources, lender risk frameworks, and repayment mechanisms that collectively define construction equipment financing in Africa. An investor or contractor also needs to research the best banks for equipment financing in Africa and the different levels of financial flexibility they offer, depending on the need and expectation.

Across African markets, financing is shaped by a combination of macroeconomic factors, including inflation, currency volatility, and limited credit access. As a result, machinery financing in Africa has evolved into a hybrid ecosystem that blends traditional banking, asset-backed lending, leasing models, and institutional capital. Understanding this ecosystem is essential for contractors seeking the best financing options for heavy equipment in Africa, as each structure carries distinct cost implications, risk exposure, and operational flexibility.

What is Equipment Financing?

Equipment financing is a structured financial solution that enables contractors to acquire construction machinery without making a full upfront capital payment. However, within the African context, the concept extends significantly beyond simple borrowing.

Contractors must align financing structures with:

- Project cash flow cycles.

- Equipment utilisation rates.

- Currency exposure.

- Maintenance and operational costs.

At its core, construction equipment financing in Africa revolves around three primary structures:

- Loans: Capital is borrowed from financial institutions and repaid over time with interest, forming the foundation of heavy equipment loans in Africa.

- Leasing: Contractors pay for equipment usage over a defined period without immediate ownership, a rapidly growing model in equipment leasing in Africa.

- Asset financing: The equipment itself serves as collateral, enabling easier access to funding in Africa.

These financial structures collectively enable contractors to bridge the gap between limited capital and high equipment costs.

A defining characteristic of machinery financing in Africa is the integration of risk mitigation mechanisms. Given the higher perceived risk in African markets, lenders typically incorporate the following:

- Collateralisation of equipment and additional assets.

- Insurance-backed financing structures.

- Revenue-linked repayment models tied to project cash flows.

- Conservative loan-to-value (LTV) ratios, often between 60% and 90%.

These mechanisms ensure capital protection while still enabling contractors to access financing.

From a strategic standpoint, contractors must evaluate how each structure aligns with their operational model. For example, high-utilisation contractors benefit more from ownership-based structures, while project-based contractors often prefer leasing arrangements.

Key Financing Models

Understanding financing models is critical when determining how to finance construction equipment in Africa step by step. Each model allocates risk differently between the lender and the borrower, influencing approval rates, the cost of capital, and long-term financial outcomes.

1. Debt Financing

Debt financing remains the dominant model in construction equipment financing in Africa, particularly through heavy equipment loans in Africa provided by commercial banks and financial institutions.

In this structure, contractors receive capital upfront and repay it over a fixed period with interest.

Key characteristics include the following:

- Fixed or variable interest rates, depending on market conditions.

- Structured repayment schedules aligned with loan tenure.

- Collateral requirements often include the equipment itself and additional assets.

Debt financing is most suitable for contractors with:

- Strong credit profiles.

- Stable and predictable cash flows.

- Established project pipelines with secured contracts.

However, the limitations of debt financing in Africa are significant. High interest rates, stringent lending criteria, and limited access for SMEs restrict its widespread applicability. This is why many contractors explore alternative structures within affordable equipment financing options in Africa.

2. Asset-Backed Financing

Asset-backed financing represents one of the most practical solutions within machinery financing in Africa, particularly for contractors with limited access to traditional bank loans.

In this model, the equipment being financed serves as the primary collateral. This reduces lender risk and improves accessibility for borrowers with weaker balance sheets.

Key advantages include the following:

- Lower entry barriers compared to unsecured loans.

- Faster approval timelines due to reduced risk assessment complexity.

- Reduced dependence on corporate financial strength.

For lenders, this structure provides security through asset recovery in the event of default. For contractors, it provides a viable pathway to scale operations. Asset financing in Africa is particularly effective in markets where credit systems are underdeveloped, as it relies more on asset value than borrower history.

However, contractors must also consider the following:

- Depreciation risks affecting collateral value.

- Strict repossession terms in case of default.

- Potential limitations on resale or transfer of financed equipment.

When applied correctly, asset-backed financing becomes a cornerstone of how contractors finance machinery in Africa, particularly for growing firms transitioning into larger projects.

3. Hybrid Financing Models

The African construction financing landscape increasingly relies on hybrid structures that combine multiple financing approaches. These models reflect the need for flexibility in environments characterised by uncertainty and capital constraints.

Common hybrid strategies include:

- Combining bank loans with leasing agreements.

- Integrating vendor/OEM financing with asset-backed loans.

- Structuring project-based financing alongside equipment leasing.

These blended approaches allow contractors to optimise cost, manage risk, and improve cash flow efficiency.

For example:

- A contractor may lease equipment for short-term projects while using loans to acquire core machinery.

- Another contractor may combine OEM financing with bank loans to reduce upfront costs.

This hybridisation is a defining feature of construction equipment financing in Africa, as it allows contractors to tailor financing structures to specific project and operational needs.

For a deeper breakdown of financing institutions supporting these models, refer to:

Best Equipment Financing Banks in Africa: 15 Trusted Banks

Key Factors to Consider Before Financing Equipment

Selecting the right financing structure is one of the most critical decisions for financing construction equipment in Africa. Contractors must evaluate financial, operational, and macroeconomic variables to ensure long-term profitability and sustainability.

Each factor below directly influences the effectiveness of construction equipment financing in Africa, particularly in high-risk, high-cost environments.

1. Interest Rates and Total Cost of Capital

Interest rates represent the most visible component of financing, but the total cost of capital extends beyond nominal rates. Contractors must evaluate the full financial burden associated with borrowing.

In African markets, interest rates are influenced by:

- Inflation and monetary policy.

- Country risk and sovereign credit ratings.

- Currency stability.

- Liquidity conditions in local banking systems.

For example, in markets such as Ghana and Zambia, lending rates can exceed 20%, significantly increasing total financing costs.

Contractors must assess the following:

- Effective annual interest rates (APR).

- Processing and administrative fees.

- Insurance costs linked to financing.

- Total repayment obligations over the loan tenure.

A comprehensive cost analysis ensures alignment with affordable equipment financing options in Africa and prevents hidden cost escalation.

2. Loan Tenure and Repayment Flexibility

Loan tenure directly impacts both cash flow management and total financing cost. Contractors must balance repayment pressure against long-term affordability.

Short-term loans:

- Reduce total interest payments.

- Increase monthly repayment burden.

Long-term loans:

- Improve cash flow flexibility.

- Increase total financing cost.

In construction equipment financing in Africa, repayment flexibility is equally important. Given the prevalence of delayed payments in construction projects, rigid repayment schedules can create liquidity stress.

Contractors should prioritise financing structures offering the following:

- Grace periods during project mobilisation

- Balloon payment options

- Revenue-linked repayment schedules

Flexible structures improve financial resilience and reduce default risk.

3. Equipment Lifecycle and Depreciation

Heavy construction equipment depreciates rapidly, particularly under harsh operating conditions common across African construction environments.

Contractors must align financing terms with:

- Equipment useful life.

- Expected utilisation rates.

- Maintenance cycles.

Failure to align these factors results in:

- Negative equity positions.

- Reduced resale value.

- Lower return on investment.

For example, financing a machine over seven years when its optimal economic life is five years creates a financial mismatch that erodes profitability. Therefore, understanding depreciation dynamics is essential when evaluating the best financing options for heavy equipment in Africa.

4. Currency and Inflation Risks

Currency volatility is one of the most significant risks in heavy equipment loans in Africa. Many financing agreements are denominated in USD or EUR, while contractor revenues are generated in local currencies.

When local currencies depreciate:

- Loan repayment costs increase.

- Profit margins shrink.

- Financial stress intensifies.

Contractors must mitigate these risks through:

- Local currency financing, where available.

- Currency hedging strategies.

- Inflation-adjusted pricing in contracts.

Inflation further compounds these challenges by increasing operating costs and reducing real income. Effective risk management is critical in ensuring the sustainability of machinery financing in Africa.

5. Ownership vs Leasing Decisions

The decision between ownership and leasing remains central to construction equipment loans vs leasing in Africa. This decision influences capital allocation, operational flexibility, and long-term financial performance.

Ownership advantages:

- Asset accumulation and balance sheet strengthening.

- Lower long-term cost for high-utilisation equipment.

- Greater operational control.

Leasing advantages:

- Lower upfront capital requirements.

- Flexibility for short-term or project-based use.

- Reduced maintenance responsibility in some agreements.

The optimal choice depends on:

- Project duration and pipeline stability.

- Equipment utilisation rates.

- Financial capacity and risk tolerance.

Contractors focused on long-term growth and asset accumulation typically prioritise ownership through loans or asset financing, while those operating in short-term or uncertain project environments often prefer equipment leasing.

How to Finance Construction Equipment in Africa: Step-by-Step Guide

Executing how to finance construction equipment in Africa step by step requires a structured, data-driven approach that integrates financial planning, risk assessment, and operational alignment. Contractors that treat financing as a process rather than a transaction consistently achieve better capital efficiency, lower borrowing costs, and higher equipment utilisation.

Across African markets, the difference between successful and struggling contractors often lies in how well they execute each stage of this process. This section provides a detailed, field-tested framework used in construction equipment financing in Africa.

Step 1: Assess Equipment Needs

The first step in financing construction equipment in Africa, step by step, is defining precise equipment requirements. This goes beyond identifying machine type. It involves aligning equipment selection with project specifications, operational capacity, and long-term utilisation.

Contractors must evaluate the following:

- Equipment type (excavators, graders, loaders, cranes).

- Capacity and specifications (tonnage, horsepower, output).

- Project duration and intensity of use.

- Terrain and environmental conditions.

For example:

A contractor operating in road construction in Tanzania may require motor graders with high durability for rough terrain, while an urban contractor in Rwanda may prioritise compact equipment for confined sites.

Incorrect equipment selection leads to the following:

- Underutilisation.

- Increased maintenance costs.

- Reduced ROI.

In the context of machinery financing in Africa, lenders increasingly assess whether the selected equipment aligns with the contractor’s project pipeline. Poor alignment can result in financing rejection or unfavourable terms.

Step 2: Evaluate Financial Position

A comprehensive financial assessment is central to financing construction equipment in Africa. Contractors must determine their borrowing capacity and financial resilience before approaching lenders.

Key financial indicators include the following:

- Cash flow stability.

- Existing debt obligations.

- Profit margins.

- Working capital levels.

Lenders offering heavy equipment loans in Africa typically assess the following:

- Debt-to-equity ratio.

- Historical financial performance.

- Project backlog.

According to the International Finance Corporation, Micro, Small, and Medium-sized Enterprises (MSMEs) in emerging markets often face financing constraints due to limited financial documentation and weak credit profiles.

To improve access to affordable equipment financing options in Africa, contractors should:

- Maintain audited financial statements.

- Demonstrate consistent revenue streams.

- Reduce existing debt exposure.

A strong financial profile directly improves:

- Loan approval probability.

- Interest rate negotiation power.

- Access to longer tenures.

Step 3: Compare Financing Options

Comparing financing structures is one of the most critical steps in financing construction equipment in Africa step by step. Contractors must evaluate the trade-offs between loans, leasing, and asset financing.

This stage directly informs decisions on construction equipment loans vs. leasing in Africa, with long-term implications for costs, flexibility, and ownership.

Key comparisons include:

Loans

- Higher upfront commitment.

- Immediate ownership.

- Lower long-term cost if utilisation is high.

Leasing

- Lower upfront cost.

- Flexibility for short-term projects.

- Potentially higher total cost over time.

Asset Financing

- Easier access due to collateral.

- Balanced risk between lender and borrower.

For contractors seeking the best financing options for heavy equipment in Africa, the decision should be based on:

- Project duration.

- Equipment utilisation rate.

- Cash flow predictability.

For example, high-utilisation equipment used across multiple projects typically justifies ownership through loans, while project-specific equipment may be better suited to leasing.

Step 4: Identify Lenders

Identifying the right financing partner is a strategic decision in construction equipment financing in Africa. Different lenders offer varying terms, risk appetites, and financing structures.

Primary financing sources include:

- Commercial banks.

- Leasing companies.

- OEM financing providers.

- Development Finance Institutions.

Institutions such as the African Development Bank and the Trade and Development Bank play a critical role in supporting infrastructure-related financing.

Each lender type has distinct characteristics:

Commercial Banks

- Structured loans.

- Higher interest rates.

- Strict collateral requirements.

Leasing Firms

- Flexible terms.

- Faster approvals.

- Focus on SMEs.

OEM Financing

- Bundled equipment + financing.

- Competitive rates.

- Maintenance support.

Contractors exploring where to finance construction equipment in Africa must align lender selection with:

- Project scale.

- Financial capacity.

- Risk tolerance.

Step 5: Prepare Documentation

Documentation quality directly affects success in financing construction equipment in Africa. Incomplete or poorly prepared documentation remains one of the leading causes of loan rejection.

Core documentation includes the following:

- Audited financial statements.

- Business plans.

- Equipment specifications.

- Project contracts and pipeline.

Lenders assess:

- Revenue visibility.

- Repayment capacity.

- Asset valuation.

In machinery financing in Africa, documentation also serves as a risk mitigation tool for lenders, particularly in markets with limited credit data.

Contractors who invest in strong documentation benefit from:

- Faster approval timelines.

- Better financing terms.

- Increased lender confidence.

Step 6: Apply and Negotiate Terms

Application and negotiation determine the final financing cost structure. Contractors must approach this stage strategically to secure affordable financing for equipment in Africa.

Key negotiation variables include the following:

- Interest rates.

- Repayment schedules.

- Grace periods.

- Collateral requirements.

In heavy equipment loans in Africa, even small reductions in interest rates can significantly reduce total repayment costs over multi-year tenures.

Contractors should:

- Compare multiple lenders.

- Leverage competitive offers.

- Negotiate flexible repayment structures.

This stage is particularly critical in volatile markets where economic conditions can change rapidly.

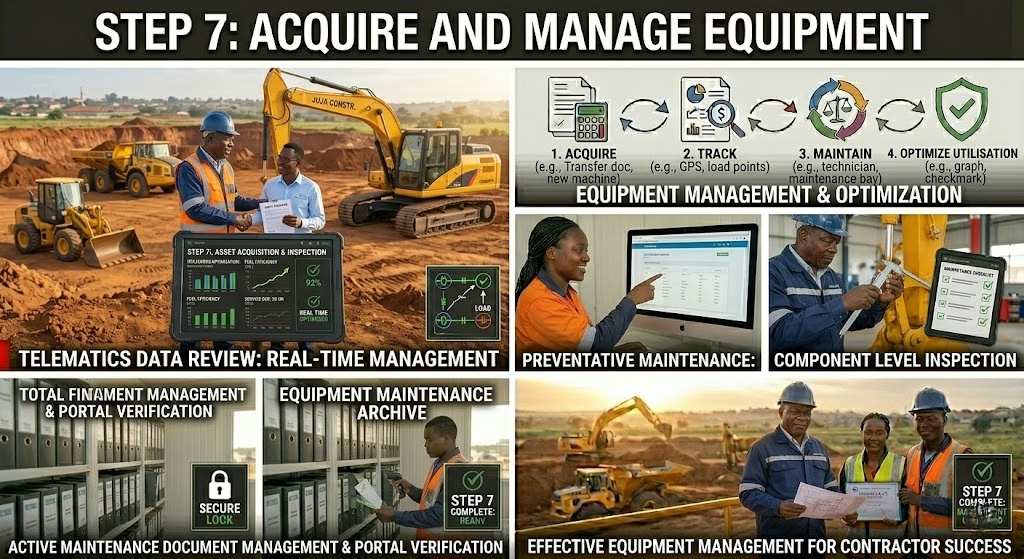

Step 7: Acquire and Manage Equipment

The final stage in how to finance construction equipment in Africa step by step extends beyond acquisition. Effective equipment management determines whether financing delivers the expected return.

Key performance metrics include the following:

- Equipment utilisation rate (target ≥75%).

- Maintenance costs.

- Revenue generated per asset.

Poor equipment management leads to the following:

- Increased downtime.

- Reduced profitability.

- Difficulty servicing debt.

Contractors must implement the following:

- Preventive maintenance schedules.

- Performance tracking systems.

- Operator training programmes.

In construction equipment financing in Africa, lenders increasingly monitor asset performance, particularly in asset-backed financing structures.

The 7 Proven Equipment Financing Options in Africa

Understanding the best financing options for heavy equipment in Africa requires a granular evaluation of each financing structure, including costs, risk allocation, approval criteria, and operational impacts. Contractors who master financing construction equipment in Africa do not rely on a single option. They strategically combine multiple financing models to optimise capital efficiency and project execution.

Across the continent, construction equipment financing in Africa continues to evolve, with increasing participation from banks, leasing firms, OEMs, and institutional investors. Each option below represents a distinct pathway within machinery financing in Africa, with specific advantages depending on contractor size, project type, and financial capacity.

1. Bank Loans (Traditional Financing)

Heavy equipment loans in Africa remain the most established and widely used financing structure, particularly among mid-sized and large contractors with proven financial track records.

In this model, contractors borrow capital from commercial banks or financial institutions to purchase equipment outright. The borrower assumes ownership immediately while repaying the loan over a fixed tenure with interest.

Advantages:

- Full ownership of the equipment from the outset, allowing asset accumulation and balance sheet strengthening.

- Predictable repayment schedules, which enable structured financial planning and cost forecasting.

- Potential tax benefits depending on jurisdiction, as depreciation can be claimed on owned assets.

Disadvantages:

- High interest rates, particularly in high-risk markets, increase the total cost of capital.

- Strict collateral requirements often include additional assets beyond the equipment itself.

- Lengthy approval processes due to detailed credit assessments and documentation requirements.

Best for: Established contractors with strong financial records, stable cash flows, and long-term equipment utilisation strategies.

From a strategic standpoint, bank loans are most effective when equipment utilisation exceeds 75% capacity, ensuring that the asset generates sufficient revenue to offset financing costs. In the context of financing construction equipment in Africa, loans are ideal for contractors focused on long-term asset ownership and expansion.

2. Equipment Leasing

Equipment leasing in Africa has emerged as one of the fastest-growing segments of construction equipment financing, particularly among SMEs and project-based contractors.

Under a leasing arrangement, contractors pay periodic fees to use equipment over a defined period. Ownership may remain with the lessor or transfer at the end of the lease, depending on the structure.

Types of Leasing:

- Operating lease: Short-term use with no ownership transfer.

- Finance lease: Long-term arrangement with an option to acquire the asset.

Advantages:

- Lower upfront capital requirements allow contractors to preserve liquidity.

- High flexibility, enabling equipment upgrades or replacements as project needs evolve.

- Reduced maintenance burden in some agreements, particularly with OEM-backed leases.

Disadvantages:

- No ownership in operating leases, limiting long-term asset accumulation.

- Higher total cost over extended periods than with an outright purchase.

- Contractual restrictions on usage, modification, or subleasing.

Best for: SMEs, short-term projects, and contractors operating in uncertain or fluctuating markets.

Leasing plays a critical role in affordable equipment financing options in Africa, as it lowers entry barriers for smaller contractors. It is also a key component of how contractors finance machinery in Africa, particularly in markets where access to credit remains limited.

3. Asset Financing

Asset financing in Africa is one of the most practical and accessible financing options, especially for contractors with weak credit histories. In this model, the equipment itself serves as collateral, reducing lender risk and improving approval rates.

This structure is widely used in machinery financing in Africa, particularly in emerging markets where traditional lending frameworks are restrictive.

Advantages:

- Easier access to financing due to reduced reliance on borrower creditworthiness.

- Faster approval timelines, as asset valuation replaces complex financial analysis.

- Lower risk for lenders, enabling more flexible financing structures.

Disadvantages:

- Strict repossession terms in case of default, which can disrupt operations.

- Depreciation risk, as declining asset value affects collateral strength.

- Limited flexibility in asset resale or transfer during the financing period.

Best for: Growing contractors seeking to scale operations without extensive financial history.

From a strategic perspective, asset financing in Africa bridges the gap between SMEs and large-scale contractors. It enables firms to transition into higher-value projects by enabling access to equipment that would otherwise be unaffordable.

4. Vendor/OEM Financing

Vendor or OEM financing represents a rapidly expanding segment within construction equipment financing in Africa, driven by global equipment manufacturers seeking to increase market penetration.

In this model, contractors obtain financing directly from equipment suppliers, often bundled with maintenance services, warranties, and technical support.

Advantages:

- Competitive interest rates due to manufacturer-backed financing.

- Integrated service packages, including maintenance and spare parts.

- Simplified procurement process, combining equipment purchase and financing.

Disadvantages:

- Limited flexibility, as financing is tied to specific brands or suppliers.

- Potentially higher equipment costs embedded within financing packages.

- Dependence on supplier networks for servicing and support.

Best for: Contractors purchasing new equipment and seeking integrated financing solutions.

OEM-backed financing is transforming how contractors finance machinery in Africa, particularly as Chinese and global manufacturers expand aggressively across the continent. By offering captive finance models, these manufacturers bypass traditional banking hurdles, aligning perfectly with the demand for affordable equipment financing options in Africa.

Leading the charge are industry giants like Sinotruk, which leverages its partnership with CFAO Mobility and NCBA Bank to offer up to 95% asset financing. Similarly, SANY has formalised a pan-African agreement with Standard Bank to provide tailored credit solutions in South Africa, Ghana, and Zimbabwe. FAW Trucks also provides competitive entry points through TransAfrica Motors, often bundling maintenance contracts with low-interest loans. These bundled services significantly reduce total lifecycle costs, making it easier for contractors to scale their fleets while maintaining healthy cash flow.

5. Development Finance Institutions (DFIs)

Development finance institutions play a critical role in construction equipment financing in Africa, particularly for large-scale infrastructure projects. Key institutions include the African Development Bank (AfDB) and the Trade and Development Bank. These institutions provide long-term financing designed to support economic development and infrastructure expansion.

Advantages:

- Lower interest rates than those of commercial banks.

- Longer loan tenures, often exceeding 10 years.

- Alignment with large infrastructure projects and government-backed initiatives.

Disadvantages:

- Complex approval processes involve extensive due diligence.

- Limited accessibility for SMEs due to scale requirements.

- Longer disbursement timelines.

Best for: Large contractors involved in infrastructure megaprojects.

DFIs are central to addressing Africa’s infrastructure financing gap, making them a key pillar for financing construction equipment for high-value projects.

6. Private Equity and Investment Funds

Private equity financing offers an alternative to machinery financing in Africa, focusing on equity participation rather than debt. In this model, investors provide capital in exchange for ownership stakes or profit-sharing arrangements.

Advantages:

- Access to large pools of capital for expansion.

- Reduced debt burden, as financing does not require fixed repayments.

- Strategic support from investors, including operational and financial expertise.

Disadvantages:

- Ownership dilution reduces control over the business.

- Pressure to deliver high returns within defined timeframes.

- Potential misalignment between investor and contractor objectives.

Best for: High-growth contractors seeking rapid expansion.

Private equity is increasingly playing a role in how contractors finance machinery in Africa, particularly in large-scale, high-growth construction firms.

7. Hire Purchase Financing

Hire purchase financing is one of the most widely adopted models within affordable equipment financing options in Africa, particularly among SMEs. Under this structure, contractors acquire equipment through instalment payments, with ownership transferring after full repayment.

Advantages:

- Predictable payment structures, enabling easier financial planning.

- Gradual ownership acquisition, reducing upfront capital requirements.

- Accessibility for smaller contractors with limited credit history.

Disadvantages:

- Higher total cost compared to outright purchase due to interest.

- Ownership only transfers after full repayment, limiting early asset leverage.

- Risk of repossession in case of missed payments.

Best for: SMEs and contractors seeking structured, accessible financing solutions.

Hire purchase remains a cornerstone of construction equipment financing in Africa, particularly in markets where leasing and bank loans are less accessible.

Explore supplier ecosystems here: 22 Best Chinese Tipper Truck Dealers in Africa: Verified List of Trusted Suppliers

Construction Equipment Loans vs Leasing in Africa

Understanding construction equipment loans vs leasing in Africa is essential for contractors aiming to optimise financial performance and operational flexibility. The choice between these two structures directly impacts capital allocation, risk exposure, and long-term profitability.

| Feature | Loans | Leasing |

| Ownership | Immediate ownership upon purchase. | Ownership at end of term or none, depending on lease type. |

| Upfront Cost | High initial capital or deposit required. | Low upfront cost, preserving liquidity. |

| Flexibility | Moderate flexibility with fixed terms. | High flexibility, especially for short-term needs. |

| Maintenance | Full responsibility lies with the owner. | Often included in leasing agreements. |

Challenges in Financing Construction Equipment in Africa

Understanding the constraints within construction equipment financing in Africa is essential for contractors seeking to scale operations sustainably. While demand for heavy machinery continues to grow, structural barriers still limit access to capital, increase financing costs, and introduce significant risk.

These challenges directly affect how construction equipment is financed in Africa, particularly for SMEs and contractors operating in volatile economic environments.

1. High Interest Rates

High borrowing costs remain one of the most critical barriers to heavy equipment loans in Africa. Interest rates are significantly higher than global averages due to macroeconomic and institutional factors.

Key drivers of high interest rates include:

- Persistent inflation across several African economies.

- Perceived country and credit risk by lenders.

- Limited liquidity in domestic banking systems.

- Weak credit infrastructure in emerging markets.

In countries such as Nigeria and Ghana, commercial lending rates can exceed 20%, thereby substantially increasing the total financing cost. For contractors evaluating affordable equipment financing options in Africa, high interest rates reduce profitability and extend payback periods, making financial planning more complex.

2. Currency Volatility

Currency risk is a defining feature of machinery financing in Africa, particularly for imported equipment financed in foreign currencies. Most heavy equipment loans in Africa are denominated in USD or EUR, while revenues are earned in local currencies. This creates exposure to exchange rate fluctuations.

Key impacts of currency volatility include:

- Increased repayment costs when local currencies depreciate.

- Reduced profit margins and financial predictability.

- Difficulty aligning project revenue with loan obligations.

Contractors operating in Kenya or Zambia frequently experience currency pressure, which directly affects the sustainability of construction equipment financing in Africa.

3. Limited SME Access to Financing

Small and medium-sized contractors face systemic barriers in accessing construction equipment financing in Africa. Financial institutions often prioritise larger firms with stronger balance sheets and established credit histories.

SMEs typically encounter:

- Strict collateral requirements beyond equipment value.

- Limited access to long-term financing structures.

- Higher perceived credit risk by lenders.

As a result, many SMEs rely on the following:

- Short-term leasing arrangements.

- Informal or high-cost financing channels.

- Equipment rental instead of ownership.

This restricts their ability to compete for large projects and limits growth within machinery financing in Africa.

4. Regulatory and Institutional Barriers

Regulatory complexity remains a persistent obstacle to financing construction equipment in Africa. The efficiency of financing systems varies significantly across countries.

Key regulatory challenges include the following:

- Lengthy loan approval processes.

- Inconsistent enforcement of collateral and repossession laws.

- Bureaucratic inefficiencies within financial institutions.

- Limited integration between financial and legal systems.

These barriers increase transaction costs and reduce the efficiency of construction equipment financing in Africa, particularly for cross-border projects.

Opportunities in Africa’s Equipment Financing Market

Despite existing challenges, Africa offers one of the most compelling environments for construction equipment financing. Contractors who understand and leverage these opportunities can significantly improve their competitive positioning.

1. Infrastructure Investment Boom

Africa’s infrastructure deficit continues to drive large-scale investment across transport, energy, and urban development sectors.

Key drivers of demand include:

- Government-led infrastructure programmes.

- Multilateral financing from institutions like the African Development Bank.

- Increased private sector participation in construction projects.

This sustained demand directly increases the need for financing construction equipment in Africa, as contractors must secure machinery to execute projects efficiently.

2. Rapid Urbanisation

Urbanisation across Sub-Saharan Africa is accelerating at an unprecedented rate, driving continuous demand for construction services.

This creates opportunities within machinery financing in Africa, including:

- Expansion of residential construction projects.

- Growth in transport and logistics infrastructure.

- Increased demand for commercial and industrial developments.

As urban populations grow, so does the demand for equipment, making financing a critical enabler.

3. Expansion of Machinery Financing in Africa

The financing ecosystem is becoming more competitive and diversified, improving access for contractors.

Key developments include the following:

- Entry of new leasing companies and fintech lenders.

- Increased availability of asset-backed financing structures.

- Expansion of OEM financing programmes.

These developments enhance affordable equipment financing options in Africa, making it easier for contractors to access capital.

4. Growth of Digital Lending Platforms

Digital innovation is transforming how construction equipment is financed in Africa by improving efficiency and accessibility.

A leading example is Moove, which operates in Nigeria and South Africa, using a “drive-to-own” model that leverages real-time revenue data to provide vehicle financing for transport and logistics entrepreneurs. In the industrial space, Solarise Africa provides decentralised equipment leasing across Rwanda, Uganda, and Kenya, using smart metering and performance data to finance solar and industrial machinery for SMEs.

Key benefits of digital lending include:

- Faster loan processing and approvals.

- Data-driven credit assessment models.

- Reduced reliance on traditional collateral structures.

This trend is particularly beneficial for SMEs, enabling broader participation in construction equipment financing in Africa.

Explore equipment demand trends: Top 5 Chinese Tipper Trucks Dominating Africa and Emerging Markets

Africa and Emerging Markets’ Financial Perspective

Placing construction equipment financing in Africa within a global context highlights both its challenges and its strategic advantages compared to other emerging regions.

1. Higher Financing Costs

Compared to Southeast Asia and Latin America, Africa experiences higher borrowing costs.

Key reasons include:

- Elevated risk perception among global investors.

- Currency instability and inflation pressures.

- Underdeveloped financial markets.

This increases the cost of heavy equipment loans in Africa, requiring contractors to adopt more efficient financing strategies.

2. Higher Return Potential

Despite higher costs, Africa offers strong return potential due to:

- High demand for infrastructure development.

- Limited competition in certain markets.

- Rapid economic growth in key regions.

Contractors who optimise financing for construction equipment in Africa can achieve strong margins and long-term growth.

3. Greater Infrastructure Demand

Africa’s infrastructure demand exceeds that of most emerging regions, creating sustained opportunities for contractors.

This drives:

- High equipment utilisation rates.

- Continuous project pipelines.

- Increased demand for the best financing options for heavy equipment in Africa.

This demand reinforces the strategic importance of financing in the construction sector.

Future Trends in Construction Equipment Financing in Africa

The future of construction equipment financing in Africa will be shaped by technological innovation, evolving capital markets, and sustainability priorities.

1. AI-Driven Credit Scoring

Artificial intelligence is transforming credit assessment within machinery financing in Africa.

Key applications include the following:

- Real-time analysis of financial and operational data.

- Improved risk profiling for contractors.

- Increased access to financing for underserved segments.

AI-driven models reduce reliance on traditional credit metrics, expanding access to affordable equipment financing options in Africa.

2. Digital Lending Expansion

Digital platforms are redefining how construction equipment is financed in Africa.

Key impacts include:

- Streamlined application processes.

- Faster disbursement timelines.

- Lower administrative costs for lenders and borrowers.

This trend is accelerating access to financing across the continent.

3. Growth of Leasing Markets

Leasing is expected to dominate future growth in construction equipment financing in Africa.

Key drivers include:

- Demand for flexible financing structures.

- Lower upfront capital requirements.

- Increased participation from OEMs and leasing firms.

This strengthens the role of equipment leasing in Africa as a scalable solution.

4. Sustainable and Green Financing

Sustainability is becoming a critical factor in financing decisions.

Emerging trends include:

- Financing for low-emission equipment.

- Incentives for energy-efficient machinery.

- Alignment with global ESG standards.

Green financing will reshape how construction equipment is financed in Africa, particularly for large infrastructure projects.

Expert Tips for Securing Equipment Financing

Successfully navigating the financing of construction equipment in Africa requires a disciplined, strategic approach.

1. Improve Creditworthiness

Contractors should prioritise financial discipline by:

- Maintaining accurate and audited financial records.

- Ensuring consistent cash flow management.

- Reducing existing debt levels.

A strong credit profile improves access to heavy equipment loans in Africa and hence reduces borrowing costs.

2. Build Lender Relationships

Establishing strong relationships with lenders provides strategic advantages.

Key benefits include the following:

- Improved trust and credibility.

- Access to preferential financing terms.

- Faster approval processes.

Relationship-building is a critical factor in successful construction equipment financing in Africa.

3. Diversify Financing Sources

Relying on a single financing source increases risk exposure.

Contractors should combine:

- Loans.

- Leasing.

- Asset financing.

This approach reflects how contractors finance machinery in Africa effectively in real-world scenarios.

4. Negotiate Favourable Terms

Negotiation plays a critical role in reducing financing costs.

Key areas to negotiate include:

- Interest rates.

- Repayment schedules.

- Collateral requirements.

Even marginal improvements can significantly impact total financing costs.

Core Financing Metrics: Your Fleet Performance Dashboard

When securing equipment loans in Africa, lenders use specific health markers to determine your creditworthiness and the viability of your project.

- Loan-to-Value Ratio (LTV) | Target: 60% – 90%

The LTV represents the percentage of the truck’s price the bank will cover. While a 90% LTV reduces your initial cash deposit, it significantly increases your monthly repayment risk. Most Sinotruk or FAW dealers in Kenya and Nigeria suggest an 80% LTV to balance upfront costs with manageable debt.

- Debt Service Coverage Ratio (DSCR) | Target: ≥ 1.2

This is the primary indicator of your ability to meet debt obligations from project cash flow. A ratio of 1.2 means you generate $1.20 in net income for every $1.00 of loan payment. If your infrastructure project’s earnings fall below this threshold, most commercial banks will view the loan as high risk.

- Equipment Utilisation Rate | Target: 75% – 85%

To maintain a positive cash flow on a financed asset, a tipper truck must be active at least 22 days per month. If your utilisation drops below 70%, the truck is likely costing more in interest and insurance than it is earning in site fees.

- Maintenance Cost Ratio | Target: 10% – 15% Annually

This ratio tracks the cost of parts and labour relative to the truck’s current value. Maintaining this within 15% is critical for lifecycle viability. Accessing authorised spare parts through dealers is the most effective way to keep this ratio from spiking.

- Payback Period | Target: 2 – 5 Years

This is the timeframe in which the truck “pays for itself”. For Chinese tippers, a 3-year payback period is the “sweet spot” enabling the contractor to achieve full ROI before major midlife overhauls (such as engine or hydraulic rebuilds) are required.

Conclusion: Mastering How to Finance Construction Equipment in Africa

Mastering how to finance construction equipment in Africa requires more than selecting a financing option. It demands a strategic approach that aligns capital structure with operational realities, project pipelines, and long-term growth objectives. Contractors who leverage construction equipment financing in Africa effectively can unlock scalability, improve cash flow resilience, and strengthen their competitive position in a capital-intensive market.

Looking ahead, the evolution of construction equipment financing in Africa will be driven by digital transformation, institutional capital flows, and increasingly sophisticated financing models. Contractors who adopt diversified financing strategies, embrace innovation, and manage risk proactively will not only secure equipment but also position themselves as leaders in Africa’s infrastructure expansion.

Stay Updated on Construction Financing Insights

Stay ahead with expert insights on how to finance construction equipment in Africa, construction equipment financing in Africa, and industry trends at Construction Frontier.