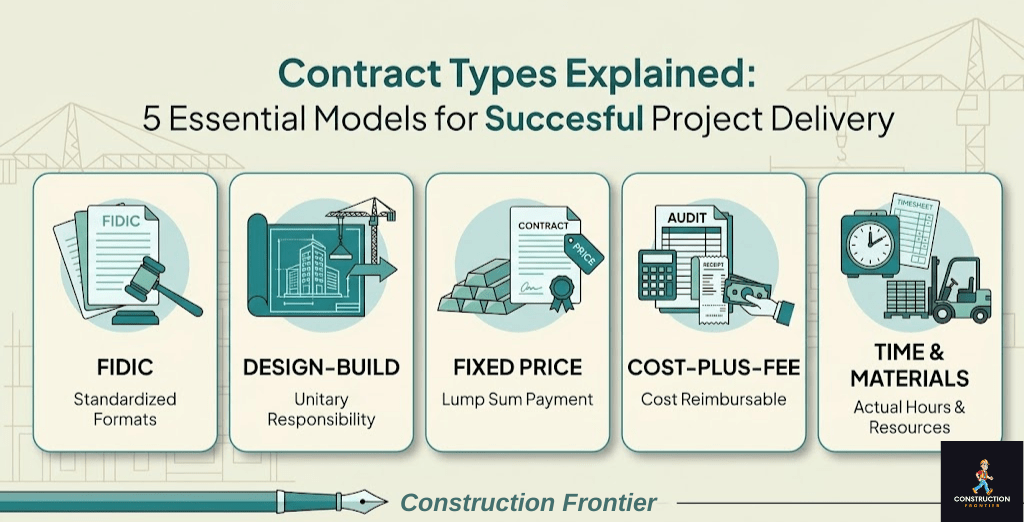

Contract Types Explained: 5 Essential Models from FIDIC to Design-Build for Successful Project Delivery

Contract types explained: every infrastructure project begins with a contractual framework that determines who assumes financial risk, how scope changes are managed, and whether a delayed handover triggers penalties or negotiations. The five primary construction contract types: Lump Sum, Cost-Plus, Time and Materials, Unit Price, and Guaranteed Maximum Price (GMP) each encode a distinct commercial philosophy, and the choice between them influences capital exposure from concept to commissioning. For mega projects, the wrong contract is not merely an administrative misstep; it is a structural liability that compounds across multi-billion-dollar programmes and multidecade concession periods.

Technical Snapshot: Core Contract Type Specifications

| Attribute | Detail |

| Primary models | Lump Sum, Cost-Plus, Time & Materials, Unit Price, GMP |

| Key international standard | FIDIC Rainbow Suite (Red, Yellow, Silver, Gold, Green Books) |

| Design-build applicability | Yellow Book (FIDIC), Design-Build, EPC/Turnkey (Silver Book) |

| Risk carrier — Lump Sum | Contractor (cost overrun risk fully transferred) |

| Risk carrier — Cost-Plus / T&M | Owner (reimburses all actual costs) |

| Risk carrier — GMP | Shared: contractor absorbs overruns above the cap |

| Risk carrier — EPC | Contractor (single-point, turnkey, performance-guaranteed) |

| Risk carrier — Design-Build | Shared: owner retains more control than EPC |

| Governing body (international) | FIDIC — established 1913; 1999 Rainbow Suite globally adopted |

| Multilateral endorsement | World Bank, Asian Development Bank, European Commission |

| Primary industry use | Power, oil & gas, heavy civil, transport, water infrastructure |

Selecting the right construction contract type directly shapes capital certainty, contractor behaviour, and the dispute-resolution landscape. Understanding how FIDIC contracts interact with procurement models such as design-build and EPC is therefore non-negotiable for project sponsors, financiers, and programme managers deploying capital at scale.

Introduction: Why Contract Types Define Project Outcomes

Infrastructure delivery is, at its most fundamental level, a contracting problem. Before the first soil investigation report reaches a geotechnical desk, before a quantity surveyor prices a bill of quantities, the contractual architecture of a programme determines the incentive structure for every party downstream. Contract types, explained across five essential models, reveal a spectrum of risk transfer arrangements, from the absolute cost certainty of a lump-sum to the collaborative budget management of a GMP. Each carries distinct implications for procurement strategy, financing structures, and the likelihood of disputes.

The role of EPC contractors in mega-project delivery is inseparable from the contractual vehicles that govern their scope. Whether a programme director selects a FIDIC Red Book, negotiates a guaranteed maximum price with an integrated design-build team, or issues a cost-plus mandate for an accelerated emergency reconstruction, the payment and risk mechanism embedded in the contract will govern contractor behaviour throughout the project lifecycle. This article examines the five primary types of construction contracts, the international FIDIC framework that underpins most cross-border infrastructure procurement, and the critical practical differences between EPC and design-build delivery, giving construction professionals, financiers, and quantity surveyors the analytical tools to select the model that best aligns with their programme objectives.

For a broader view of how these frameworks slot into programme-level decision-making, the article by Construction Frontier on managing mega construction projects provides the strategic context within which contract selection operates.

The Five Primary Construction Contract Types Explained

Understanding the full range of construction contract types requires examining how each model allocates financial risk, structures payment, and responds to scope change because no single model suits every programme. The five types reviewed below span the full risk spectrum, from owner-protective cost-plus arrangements to contractor-bearing lump sum commitments, and each has a defined set of project conditions under which it performs optimally.

1. Lump Sum (Fixed Price) Contracts

A lump-sum contract, also called a stipulated sum or fixed-price contract, establishes a single, predetermined price for completing a defined scope of work. The contractor agrees to deliver the project for that sum regardless of actual labour, material, or equipment costs incurred. Under this structure, cost overrun risk transfers entirely to the contractor: if actual costs exceed the contract sum, the contractor absorbs the loss; if they fall short, the contractor retains the saving as additional margin.

Lump-sum contracts perform best when scope documentation is mature and complete before tender. Civil engineering programmes with fully designed drawings, detailed specifications, and quantified bills of quantities represent the archetypal application. Projects procured under this model, using FIDIC Red Book conditions, where the employer provides the design and the contractor executes it, typically use lump-sum or re-measurement payment structures. The primary drawback is scope sensitivity: any variation to the defined works triggers a change-order process that can lead to delay claims and commercial disputes. For the best construction contract type for infrastructure projects with well-defined, stable scopes, the lump-sum remains the benchmark for simplicity and budget certainty.

2. Cost-Plus Contracts

Cost-plus contracts require the owner to reimburse the contractor for all verifiable project costs, including labour, materials, equipment, and approved overheads, plus a predetermined fee to cover profit. The fee can be structured as a fixed sum (Cost-Plus Fixed Fee), a percentage of actual costs (Cost-Plus Percentage Fee), or a fixed fee within a guaranteed maximum (Cost-Plus GMP). Under all variants, the owner carries the majority of financial risk, since all on-site costs are transferred to the owner’s account.

This model is most effective when scope definition is genuinely impossible at the outset, in accelerated disaster recovery programmes, early-contractor-involvement (ECI) arrangements, and complex refurbishment projects where latent conditions are unknown. Cost-Plus contracts demand robust owner-side cost monitoring; without systematic open-book auditing, cost escalation can proceed unchecked.

The administrative burden is significantly higher than for lump-sum procurement, and quantity surveyors must implement rigorous cost validation protocols. Construction professionals operating on contract types explained in construction projects with evolving scopes frequently recommend pairing cost-plus with a guaranteed maximum price cap to convert owner-facing risk into a defined ceiling.

3. Time and Materials (T&M) Contracts

A Time and Materials contract reimburses the contractor for actual material costs and pays labour at agreed-upon daily or hourly rates, inclusive of overhead and profit. Unlike cost-plus, the profit mechanism is built directly into the labour rate schedule rather than applied as a separate fee. T&M contracts are structurally similar to cost-plus but differ in how contractor remuneration is engineered: T&M compensates per unit of time worked regardless of productivity, while cost-plus ties the fee more explicitly to total project expenditure.

T&M contracts suit short-duration, difficult-to-scope engagements: specialist investigative work, emergency repairs, and programme packages issued before full design completion. The commercial risk to the owner is that contractor productivity ceases to be a meaningful incentive, as slow execution results in higher billable hours. For this reason, sophisticated owners typically cap T&M exposure with a Not-to-Exceed (NTE) clause or convert the engagement to a lump sum once the scope crystallises. In choosing the right construction contract type, T&M serves as a transitional vehicle rather than a programme-level procurement strategy.

4. Unit Price Contracts

Unit price contracts divide the project scope into measurable work items, such as metres of road paving, cubic metres of earthworks, and tonnes of reinforced concrete and price each unit independently. The final contract value is calculated by multiplying the agreed unit rates by the actual quantities measured on completion. Payment reflects real-world site conditions rather than pre-estimated totals, distributing quantity risk between owner and contractor: if actual quantities exceed the bill of quantities estimates, the owner absorbs the cost of additional units; if quantities are lower, the owner benefits from the savings.

This structure is the standard procurement vehicle for heavy civil infrastructure roads, earthworks, drainage, and pipeline installation, where the scope is well understood in terms of specification but genuinely uncertain in terms of volume. The FIDIC Red Book, used globally for types of construction contracts on employer-designed civil projects, incorporates remeasurement provisions aligned with unit price principles under Clause 12. Unit price contracts demand rigorous site measurement discipline, and quantity surveyors operating in this environment must maintain continuous liaison with site engineers to avoid month-end measurement disputes that compound into programme-level claims.

5. Guaranteed Maximum Price (GMP) Contracts

A Guaranteed Maximum Price contract establishes a ceiling on the total cost the owner will pay. Below that ceiling, the project operates on a cost-plus or open-book basis; above it, the contractor absorbs the overrun. Many GMP contracts include a shared savings clause, under which any budget underspend at completion is split between owner and contractor according to an agreed ratio, creating a genuine incentive for the contractor to optimise cost performance rather than merely meet the cap.

GMP contracts are structurally more complex than lump-sum instruments and require detailed cost reporting, robust change management protocols, and mutual transparency between parties. They suit programmes where design is advanced but not fully complete, allowing construction to commence before the last design packages are issued without exposing the owner to unlimited cost escalation.

For commercial building programmes, hospital and education campus developments, and public-sector infrastructure delivered under construction management arrangements, the GMP model has become the dominant procurement vehicle. Its hybrid position between construction contract types, combining cost transparency with budget certainty, makes it the logical instrument when scope carries known uncertainty but owner exposure must be capped.

Further Reading: How EPC Project Delivery Works: 7 Proven Steps Driving Successful Infrastructure Projects

Comparative Analysis: 5 Primary Construction Contract Models

| Contract Type | Risk Allocation | Payment Structure | Advantages (Pros) | Disadvantages (Cons) |

| Lump Sum (Fixed Price) | The contractor bears most of the risk and absorbs all overruns. | Single, predetermined price for a defined scope. | High budget certainty; minimal administrative oversight. | Highly sensitive to scope changes; prone to disputes over variations. |

| Cost-Plus | The owner carries most of the risk and pays all actual costs. | Reimbursable costs plus a fixed or percentage fee. | High flexibility allows for an immediate start despite an ill-defined scope. | Final cost is unknown; requires rigorous “open-book” auditing. |

| Time & Materials (T&M) | The owner carries the risk of low productivity. | Hourly/daily labour rates plus material costs. | Ideal for small, urgent, or investigative works. | No incentive for contractor efficiency; costs can escalate quickly. |

| Unit Price | Shared: Owner carries quantity risk; Contractor carries rate risk. | Based on measured quantities of work items. | Accurate payment for actual work done; ideal for civil/road works. | Requires heavy site measurement and continuous quantity surveying. |

| Guaranteed Max Price (GMP) | Contractor bears costs exceeding the agreed cap. | Open-book cost-plus up to a defined ceiling. | Caps owner exposure; encourages efficiency via shared savings. | High administrative complexity; requires advanced (but not final) design. |

FIDIC Contracts Explained: The International Standard

The FIDIC Rainbow Suite governs the majority of cross-border infrastructure financing globally, providing a standardised contractual architecture that multilateral development banks, sovereign clients, and international contractors can negotiate within a shared framework. Understanding FIDIC contracts in practical terms requires examining not only the colour-coded book structure but also how each variant maps onto the five payment models above, and why the international financing community has endorsed FIDIC as the de facto standard for infrastructure delivery.

1. The Red Book: Employer-Designed Works

The FIDIC Conditions of Contract are the most widely used international construction contract for projects where the employer provides the design and the contractor executes. Payment is typically based on bills of quantities measured by the engineer, aligning the FIDIC Red Book naturally with unit price and re-measurement procurement. The engineer, a named third-party professional, administers the contract, certifies payments, and issues instructions, acting as the principal mechanism for balancing employer and contractor interests. Risk allocation under the Red Book is structured as a balance: the contractor carries construction risk, while the employer retains design liability.

The 1999 edition introduced the Dispute Adjudication Board (DAB) as the primary dispute resolution mechanism, a standing three-person panel empowered to issue binding decisions in real time, reducing the programme disruption that accompanies arbitration. The 2017 update reinforced this framework while strengthening obligations regarding programme and notice requirements, as well as the engineer’s neutrality in decision-making. World Bank and African Development Bank (AfDB) financing facilities routinely reference the Pink Book, the MDB harmonised edition of the Red Book, as the standard procurement instrument for their infrastructure lending portfolios.

2. The Yellow Book: Design-Build Delivery

The FIDIC Yellow Book (Conditions of Contract for Plant and Design-Build) governs contracts where the contractor assumes responsibility for both design and construction. Unlike the Red Book, where the employer provides design documentation, the Yellow Book requires the contractor to meet the employer’s performance and functional requirements, with design developed and executed under the contractor’s professional liability. Payment is typically structured as a schedule of payments rather than a re-measured bill.

The Yellow Book applies naturally to the design-build contract delivery model, the procurement method in which one entity manages design, procurement, and construction under a single integrated contract. In contrast to FIDIC contracts, the Yellow Book essentially codifies design-build risk allocation: the contractor assumes fitness-for-purpose liability for the completed works, and the employer-engineer relationship becomes less interventionist than under the Red Book.

For power sector infrastructure, water treatment facilities, and building engineering programmes, the Yellow Book has become the most commonly selected FIDIC instrument for contract types explained in construction projects where the contractor’s design capability is integral to the procurement strategy.

3. The Silver Book: EPC and Turnkey Projects

The Silver Book (Conditions of Contract for EPC/Turnkey Projects) represents the most contractor-loaded risk position within the FIDIC suite. Under the Silver Book, the EPC contractor assumes sole and total responsibility for engineering, procurement, construction, and commissioning, delivering a fully operational facility that meets the output performance criteria specified by the owner. There is no FIDIC engineer administering the contract; the employer’s representative replaces the engineer’s function, but with significantly reduced independent authority.

The Silver Book is FIDIC’s formal instrument for EPC/Turnkey procurement, and the risk transfer it encodes is comprehensive: unforeseen ground conditions, design errors, supply chain delays, and performance shortfalls all sit within the contractor’s liability envelope. This concentration of risk commands a corresponding premium in the contractor’s tender price. For industrial process facilities, power generation assets, oil and gas infrastructure, and large-scale water treatment plants where what the facility produces matters more than how it is designed, the Silver Book provides the contractual precision that multilateral lenders and project finance structures require.

4. The Green and Gold Books

The Green Book provides a streamlined, short-form contract suited to projects valued at approximately USD 500,000 or less or with construction periods of six months or less, reducing administrative overhead for straightforward scopes. The Gold Book (Design, Build and Operate) extends the contractor’s obligation beyond commissioning into a long-term operations and maintenance period, typically 20 years from the commissioning certificate, making it the appropriate FIDIC vehicle for Public-Private Partnerships (PPP) and Build-Operate-Transfer (BOT) concession structures where lifecycle performance and asset integrity over the concession period are part of the contractor’s contractual commitment.

EPC vs Design-Build Contracts: Navigating the Key Differences

The distinction between EPC vs design-build contracts is one of the most consequential decisions in infrastructure procurement, yet it remains widely misunderstood even among experienced practitioners. Both models place design and construction under a single contractual relationship, and both offer the owner a single point of accountability. The differences, however, are material: they determine how much risk the contractor assumes, how much operational involvement the owner retains, and what pricing structure governs the commercial relationship throughout the programme lifecycle.

1. Risk Allocation: The Fundamental Divergence

In a true EPC contract, the contractor assumes virtually all project risk: design liability, procurement risk (including supply chain delays and equipment cost escalation), construction execution, and final performance guarantees. The owner specifies output criteria, the required generating capacity of a power plant, the throughput of a water treatment facility, and the structural performance of a bridge, and the EPC contractor determines how to meet them. Site condition risk under EPC is typically allocated to the contractor, as is design error liability. The fixed, lump-sum pricing of most EPC contracts reflects this comprehensive risk transfer: the contractor prices its risk exposure into the tender sum.

Design-build contracts distribute risk more symmetrically. The design-builder assumes liability for design errors and construction delivery, but the owner typically retains a more active role in design approvals, scope management, and risk-sharing for unforeseen conditions. Under the FIDIC Yellow Book design-build framework, the employer’s requirements define performance outcomes but allow the contractor design flexibility, creating a collaborative dynamic that differs structurally from the arms-length performance-criteria-only approach of Silver Book EPC. Projects delivered under the wrong design-build delivery method commonly experience 20 to 50 percent cost overruns, whereas properly matched delivery methods achieve on-time completion rates exceeding 90 percent.

2. Owner Involvement and Control

EPC contracts deliberately minimise owner involvement during execution. Once the contract is awarded, the EPC contractor controls engineering decisions, procurement selections, and construction sequencing. The owner monitors milestone deliverables and performance benchmarks rather than engaging in day-to-day project management. This low-intervention model suits programme sponsors who lack in-house technical capacity or who are managing multiple concurrent capital investments; it is standard practice in the energy, oil and gas, and heavy process industries, where the facility is ultimately a production asset rather than a bespoke built environment.

Design-build preserves considerably more owner control. The owner participates in design development, reviews and approves design packages at defined stages, and retains the authority to redirect scope during execution. This engagement model suits public-sector clients, transport authorities, municipal utilities, and health boards that must demonstrate democratic accountability for design decisions and whose built assets must integrate into existing civic infrastructure. The trade-off is that greater owner involvement introduces more interface points where scope changes can be initiated, demanding robust change control disciplines to prevent cost and programme drift.

3. Pricing and Payment Structures

Most EPC contracts are executed on a Lump Sum Turnkey (LSTK) basis: a single, fixed price for a fully operational facility, with payment tied to construction milestones and final performance acceptance testing. This pricing model gives project finance lenders the cost certainty required to model debt service coverage ratios and structure loan covenants, which is why LSTK EPC is the near-universal delivery vehicle for project-financed power generation, LNG, and mining infrastructure.

Design-build contracts offer considerably more pricing flexibility. They can operate under lump-sum, GMP, cost-plus, or unit-price structures, depending on the programme stage and the degree of design maturity at contract award. Early-stage design-build procurement, where detailed design runs concurrently with construction, suits cost-plus or GMP pricing because design development inevitably generates scope evolution. As design advances toward completion, a lump sum conversion is common, transferring cost risk to the contractor once the scope is sufficiently defined. This pricing flexibility is one of the primary practical advantages of design-build contract procurement over pure EPC models for programmes with complex phased delivery requirements.

Further Reading: The Role of EPC Contractors: 10 Critical Functions Driving Successful Infrastructure Delivery

How to Choose the Right Construction Contract Type

Selecting the appropriate construction contract type from the available options requires a structured diagnostic that assesses project-specific variables before committing to a procurement strategy. Getting this decision right defines the programme’s commercial efficiency; getting it wrong creates structural vulnerabilities that become progressively more expensive to correct as construction advances.

1. Scope Definition and Design Maturity

The most reliable predictor of the right construction contract type is the maturity of the scope documentation at the time of contract award. Projects with fully designed drawings, comprehensive specifications, and stable stakeholder requirements are suited to lump-sum procurement; the fixed price reflects the contractor’s ability to accurately price a defined scope. Programmes entering procurement before design is complete should default to GMP or Cost-Plus frameworks, converting to lump sum as design packages are released and priced.

EPC procurement requires output-based employer requirements (functional performance criteria) rather than detailed design documentation; the EPC contractor prepares the detailed design. Attempting to impose EPC structures on projects with immature scope definitions invariably produces inflated contingency pricing and contractor claims.

2. Risk Tolerance and Financial Capacity

Owner risk tolerance is the second determinant. Project sponsors who require absolute budget certainty because they are operating within a fixed capital allocation, servicing project finance debt or reporting to public-sector budget controls should default to risk-transfer models: lump-sum, GMP with a hard cap, or EPC.

Owners with stronger financial flexibility and the in-house technical capacity to monitor open-book cost reports can absorb cost-plus or T&M exposure in exchange for procurement speed and scope flexibility. The FIDIC guidance on contract selection is explicit on this point: diverging significantly from the balanced risk-sharing principles embedded in standard forms typically results in higher tender prices and a higher probability of disputes.

3. Project Complexity and Sector

Industrial process facilities, power plants, petrochemical refineries, desalination plants, and LNG terminals consistently demand EPC or Silver Book structures because their primary deliverable is performance output rather than built form. The EPC contractor’s control over procurement, equipment specification, and system integration is essential to delivering the performance guarantees that define the asset’s value. Commercial and civic construction offices, hospitals, schools, and mixed-use developments typically suit design-build or GMP procurement because stakeholder-driven design iteration and aesthetic quality are legitimate programme objectives that the collaborative design-build model supports more naturally than the output-specification EPC model.

For the best construction contract types for infrastructure projects spanning civil engineering disciplines, roads, bridges, dams, and pipelines, the FIDIC Red Book with unit price remeasurement remains the international benchmark, providing balanced risk allocation and a transparent measurement framework. Heavy civil programmes funded by multilateral development banks almost universally reference FIDIC Red Book or Pink Book conditions, and procurement teams familiar with the associated engineer certification and Dispute Adjudication Boards’ (DABs) dispute resolution mechanisms will find the administrative overhead manageable relative to the risk mitigation those mechanisms provide.

Technical Block: Construction Contract Selection Reference

1. FIDIC Rainbow Suite at a Glance

| FIDIC Book | Key Application |

| Red Book (1999/2017) | Employer-designed civil works, Unit Price/re-measurement payment, balanced risk allocation, engineer-administered |

| Pink Book (MDB Harmonised) | Multilateral bank-financed projects: Red Book base with MDB-specific particular conditions |

| Yellow Book | Design-build; contractor-designed; performance specification; schedule of payments; fitness-for-purpose liability |

| Silver Book | EPC/Turnkey; single-point responsibility; fixed lump-sum; performance guarantees; no independent engineer |

| Gold Book | Design-Build-Operate (DBO): contractor operates for a 20-year concession period; lifecycle performance commitment |

| Green Book | Short Form; projects under US$500,000 or under 6 months; simplified conditions; minimal administrative burden |

2. Contract Type Risk and Complexity Matrix

| Contract Type | Cost Risk Owner | Cost Risk Contractor | Admin Complexity | Price Certainty | Best Fit Scope |

| Lump Sum | Low | High | Low | Very High | Fully defined |

| Cost-Plus | High | Low | High | None | Undefined/evolving |

| T&M | High | Low | Medium | None | Short/investigative |

| Unit Price | Medium | Medium | Medium | Medium | Civil/repeatable |

| GMP | Capped | Above-cap | High | High (capped) | Advanced design |

| EPC (LSTK) | Very Low | Very High | Contractor’s side | Very High | Output-specified |

| Design-Build | Medium | Medium-High | Shared | Medium-High | Variable |

Conclusion: Navigating the Risk of the 5 Contract Models for Guaranteed Project Delivery

Contract selection is ultimately a capital allocation decision, and the five construction contract types explained here represent five distinct theories of risk pricing. The lump-sum transfers shift risk to the contractor in exchange for a fixed, financeable price, suitable when the scope is mature, and competition is sufficient to produce a credible market rate. The GMP model introduces collaborative cost transparency while capping owner exposure, performing best when design and construction advance concurrently. Cost-Plus and T&M preserve maximum flexibility at maximum owner cost exposure, appropriate only when the scope is genuinely unquantifiable.

Unit price delivers measurement fairness on large civil programmes where quantities are variable, but unit rates are competitive. EPC, governed internationally by the FIDIC Silver Book, concentrates all risk on the contractor in exchange for a turnkey facility and a performance guarantee, the model of choice for project-financed industrial infrastructure. Understanding FIDIC contracts explained within this framework allows procurement professionals to match the contractual instrument to the programme’s commercial reality rather than defaulting to institutional inertia.

The evolution of infrastructure procurement is trending toward hybrid models: GMP with early contractor involvement, design-build with incentivised performance milestones, and EPC with partial risk-sharing on force majeure events because capital markets are increasingly sophisticated in pricing risk and financiers demand structures that neither over-incentivise contractor conservatism through excessive margin-loading nor expose sponsors to uncapped contingencies.

For construction professionals, quantity surveyors, and programme financiers operating in this environment, the ability to navigate EPC vs design-build contracts with analytical precision, understanding not merely what each model is, but how it performs under stress, how it responds to scope change, and how it aligns with the capital structure of the programme, is a core competency that separates transactional procurement from strategic infrastructure delivery. The technical and commercial dynamics of mega-project management demand nothing less.

Stay Updated on Africa’s Infrastructure Megaprojects

Stay ahead of the infrastructure transformation in Africa and emerging markets with Construction Frontier: Civil Engineering & Construction Practices. Explore deep technical insights, expert analysis, and investment intelligence shaping the future of African infrastructure procurement and project delivery.