Construction Equipment Market in Africa: 2025–2035 Growth

The construction equipment market in Africa will enter a decisive growth cycle between 2025 and 2035, driven by infrastructure expansion, mining investments, and rapid urbanisation across key regional economies. The construction equipment market forecast for 2025 to 2035 shows a transition from fragmented demand to structured, capital-backed growth supported by governments, development finance institutions, and private investors.

The Africa construction machinery market growth analysis highlights increasing equipment intensity across projects, rising mechanisation adoption, and expanding access to financing. These shifts will redefine equipment demand in Africa’s construction and position the continent as a global growth frontier.

Technical Snapshot: Market Benchmarks (2025–2035)

- Expected CAGR: 6%–8% across major African markets.

- Infrastructure-driven demand share: >55% of total equipment utilisation.

- Mining sector contribution: ~25%–30% of heavy equipment demand.

- Equipment import dependency: >70% across most countries.

- Urbanisation-driven demand growth: accelerating beyond 2030.

Introduction: The Construction Equipment Market in Africa

The construction equipment market in Africa encompasses the supply, financing, deployment, and lifecycle management of heavy machinery used across infrastructure, mining, energy, and urban development sectors. Equipment such as excavators, loaders, cranes, and road construction machinery plays a central role in delivering large-scale projects efficiently and within budget.

Across Africa, contractors increasingly rely on equipment to:

- Accelerate infrastructure delivery timelines.

- Improve productivity in mining and energy operations.

- Support rapid urban expansion and housing development.

Africa stands at a critical inflection point. Governments and institutions continue to prioritise infrastructure investment to unlock economic growth, aiming to close a massive annual financing gap estimated between $68 billion and $108 billion. The African Development Bank notes that the continent requires a total annual investment of $130 billion to $170 billion to meet its development goals by 2025.

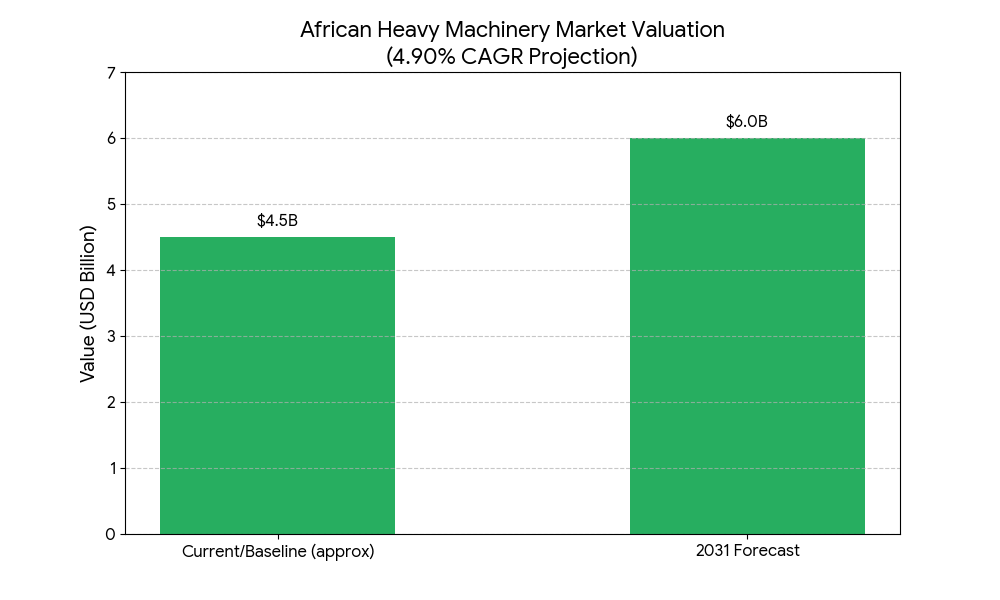

The construction equipment market in Africa is forecast to grow at a CAGR of 4.90% from 2025 to 2031, with the heavy equipment segment alone projected to reach $6.00 billion by 2031. This sustained upward trajectory is anchored by deep structural demand: 65% of Africa’s population is expected to reside in urban areas by 2050, necessitating massive investments in housing and public services. This positions Africa as one of the most attractive growth frontiers within the global construction equipment industry.

Construction Equipment Market Size and Growth Outlook (2025–2035)

The construction equipment market in Africa continues to expand as infrastructure pipelines mature and capital inflows increase. The construction equipment market in Africa is forecast to grow steadily from 2025 to 2035, supported by both public and private sector investments.

Baseline estimates for 2025 place the market at a growing but under-penetrated level relative to global benchmarks. By 2035, the Africa construction machinery market growth analysis projects a significantly larger market size, driven by sustained demand across infrastructure, mining, and urban development.

Key growth indicators include the following:

- Rising infrastructure expenditure across the transport and energy sectors.

- Increased investment in mining operations, particularly in copper and critical minerals.

- Expansion of urban construction projects driven by population growth.

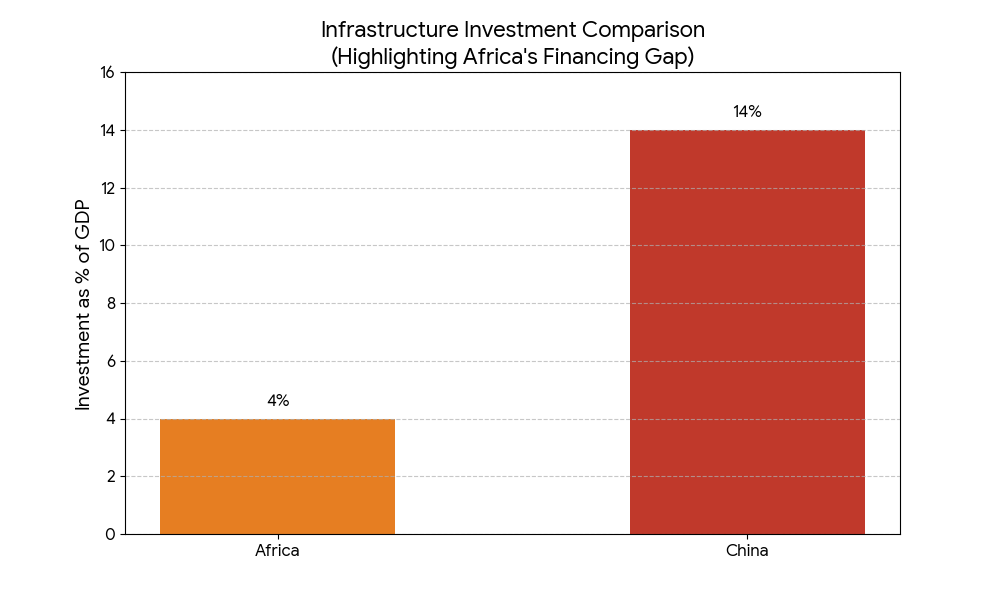

Africa’s infrastructure investment remains a primary economic driver, with bridging the continent’s infrastructure gap estimated to increase GDP growth by an additional 2 percentage points annually. Currently, Africa invests only 4% of its GDP in infrastructure compared to 14% in China, leaving an annual financing requirement of $130 billion to $170 billion to meet the 2030 development goals.

For deeper insights into equipment demand trends, explore:

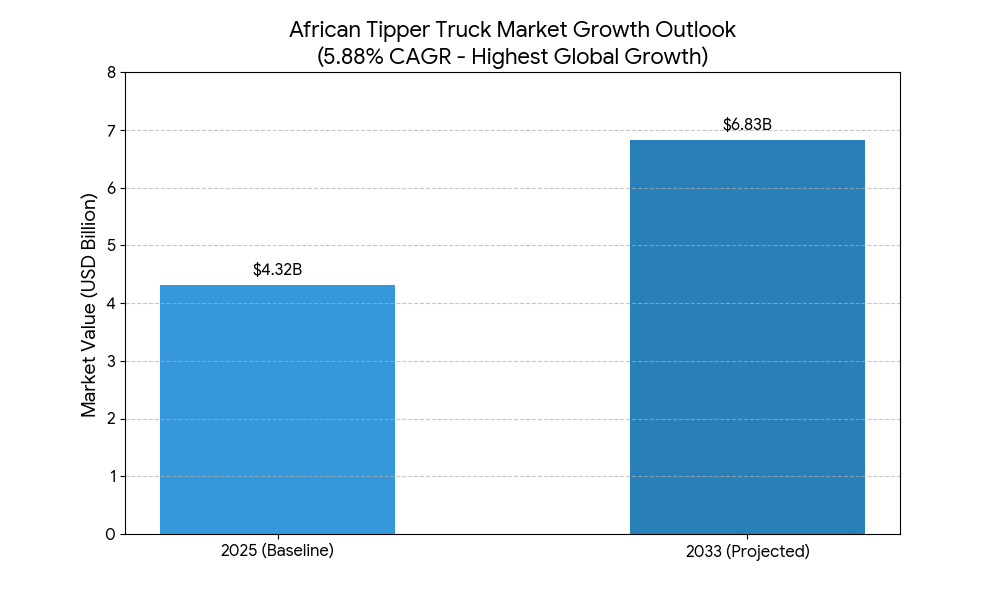

- Global Tipper Truck Market: In our Construction Frontier global tipper truck market report, we noted that insights shaping construction logistics indicate that the African tipper truck sector is outperforming global averages. Valued at $4.32 billion in 2025, it is projected to reach $6.83 billion by 2033, growing at a robust 5.88% CAGR, the highest regional growth rate globally.

- Logistics Infrastructure: Demand is further validated by a surge in industrial real estate; modern warehouse occupancy across Africa reached 83% in 2025, driven by a projected $75 billion online retail market.

The growth of the heavy equipment market in Africa will remain closely tied to infrastructure, pipelines, and the availability of financing. Strategic shifts are already visible, with over 80 development corridors currently planned or under construction to support the African Continental Free Trade Area (AfCFTA). These projects reinforce the long-term viability of the construction equipment market, which is forecast to maintain a 4.90% CAGR through 2031, reaching a valuation of $6.00 billion for heavy machinery alone.

Key Metrics for Authority (2025–2026)

| Metric | Verified Value / Forecast | |

| Annual Infrastructure Need | $130B – $170B | |

| Tipper Truck Market CAGR | 5.88% (Highest Globally) | |

| Heavy Equipment Value (2031) | $6.00 Billion | |

| Urbanisation Target (2050) | 65% of the population in cities | |

| Warehouse Occupancy (2025) | 83% (up from 75% in 2024) |

Core Drivers of Equipment Demand in Africa’s Construction Sector

The construction equipment market in Africa is driven by multiple structural factors that collectively shape long-term growth. These drivers define the trajectory of equipment demand in Africa’s construction sector and determine the pace of heavy equipment market growth.

1. Infrastructure Expansion and Mega Projects

Infrastructure development represents the most powerful driver within the construction equipment market in Africa. Governments across the continent continue to invest in roads, railways, ports, and energy infrastructure.

Key developments include the following:

- Expansion of transport corridors connecting regional economies.

- Construction of large-scale energy projects, including hydropower and renewables.

- Development of logistics hubs and industrial zones.

These projects require extensive use of earthmoving and road construction equipment, directly influencing the heavy equipment demand forecast for Africa 2035.

2. Urbanisation and Housing Demand

Africa’s urban population continues to grow rapidly, creating sustained demand for housing and urban infrastructure. This trend is driving the construction machinery market in Africa, particularly in the mid-size and compact equipment segments.

Key impacts include:

- Expansion of residential housing projects.

- Increased demand for construction materials and logistics.

- Growth in municipal infrastructure, such as roads and drainage systems.

Urbanisation is strengthening trends in the construction equipment industry in Africa, particularly for equipment suited to dense urban environments.

3. Mining and Natural Resource Development

Mining remains a major contributor to the construction equipment market in Africa, particularly in countries rich in natural resources, such as Zambia, the DRC, and Guinea. The demand for minerals, such as copper, lithium, and iron ore, drives heavy equipment utilisation.

The heavy equipment demand forecast for Africa 2035 highlights mining as a critical growth segment, with strong demand for high-capacity equipment such as excavators and dump trucks.

4. Regional Trade and Industrialisation

The implementation of the African Continental Free Trade Area is reshaping regional trade dynamics. Increased trade activity drives demand for logistics infrastructure and industrial facilities.

This trend supports:

- Development of industrial parks and manufacturing zones.

- Increased movement of goods across borders.

- Expansion of construction activity linked to trade infrastructure.

These developments reinforce long-term growth in the construction equipment market in Africa.

African Construction Industry Trends Shaping Equipment Markets

The African construction industry trends influencing equipment demand reflect a shift toward efficiency, mechanisation, and structured project execution. These trends in the construction equipment market in Africa will define the competitive landscape over the next decade.

Key trends include:

- Shift toward mechanisation: To improve productivity, contractors are pivoting from manual labour to high-output machinery. This is reflected in the surging demand for excavators, which accounted for 27.6% of all construction machinery exports to Africa in the first half of 2025.

- Reliance on imported machinery: African markets remain heavily reliant on imports. In H1 2025, Chinese construction machinery exports to the continent reached $4 billion, a 51.6% year-on-year increase, signalling a massive influx of new fleet capacity.

- Growth of rental and leasing markets: High interest rates are driving a preference for OpEx over CapEx. The African equipment rental market is expanding as contractors seek to preserve liquidity; global players like Sany reported a 40.5% revenue increase in Africa during 2025, largely supported by flexible local financing and leasing partnerships.

- Expansion of OEM presence: Global manufacturers are moving beyond simple sales to localised support. LiuGong and other major OEMs have recently established regional spare parts hubs in East and West Africa to reduce machine downtime, which can cost contractors up to $5,000 per day on large-scale projects.

These trends in the construction equipment industry in Africa highlight a transition toward a more structured and capital-intensive industry.

Deeper dive: Top 5 Chinese Tipper Trucks Dominating Africa and Emerging Markets

Construction Equipment Market Segmentation by Equipment Type

The construction equipment market in Africa demonstrates clear segmentation across equipment categories, each aligned with specific project phases, productivity requirements, and capital intensity levels. This segmentation reflects evolving African construction industry trends, where contractors increasingly optimise fleet compositions based on utilisation rates, terrain conditions, and lifecycle cost efficiency.

Equipment segmentation also reveals how equipment demand in Africa’s construction sector shifts with sectoral drivers such as infrastructure, mining, and urban development. The construction equipment market in Africa, forecast from 2025 to 2035, indicates that earthmoving and road construction equipment will dominate volume. Demand for material handling and concrete equipment will accelerate due to urbanisation.

1. Earthmoving Equipment

Earthmoving equipment forms the backbone of the construction equipment market in Africa, accounting for the largest share of equipment utilisation across infrastructure and mining projects. Excavators, bulldozers, wheel loaders, and motor graders dominate this segment due to their versatility and high productivity in large-scale operations.

These machines operate at the earliest stages of project execution, directly influencing project timelines and cost efficiency. Contractors rely on earthmoving equipment for:

- Bulk excavation and site clearance across transport and energy projects.

- High-volume material movement in mining operations.

- Terrain levelling and grading for road and urban development.

From a technical perspective, excavators in the 20–50 tonne range represent the most widely deployed class across African markets. This range balances power, mobility, and fuel efficiency, making it suitable for both infrastructure and mid-scale mining applications.

The heavy equipment demand forecast for Africa 2035 shows sustained growth in this segment, driven by:

- Expansion of transport corridors and logistics infrastructure.

- Increased mining activity linked to global mineral demand.

- Rising adoption of mechanised construction methods.

Contractors increasingly evaluate earthmoving equipment based on:

- Fuel consumption per operating hour.

- Bucket capacity and cycle time efficiency.

- Durability under harsh operating conditions.

This shift reflects broader trends in the construction equipment industry in Africa, where performance metrics now drive procurement decisions rather than upfront cost alone.

2. Material Handling Equipment

Material handling equipment plays a critical role in supporting vertical construction, industrial projects, and logistics operations within the construction machinery market in Africa. This segment includes tower cranes, mobile cranes, forklifts, and telehandlers, all of which facilitate efficient movement of materials within confined or high-density environments.

Urbanisation drives demand in this segment. As cities expand vertically, contractors require advanced lifting solutions to handle steel, concrete, and prefabricated components. This directly influences equipment demand in Africa’s construction, particularly in commercial and residential developments.

Cranes, especially mobile and tower configurations, dominate this category. Mobile cranes offer flexibility for infrastructure and industrial projects, while tower cranes support high-rise construction in urban centres.

Technical factors shaping this segment include the following:

- Lifting capacity and reach, which determine suitability for specific projects.

- Stability and safety systems critical in high-risk environments.

- Integration with digital load monitoring systems to improve efficiency.

Forklifts and telehandlers also play an increasingly important role in logistics and warehousing, particularly in industrial parks and special economic zones. The expansion of regional trade under the African Continental Free Trade Area increases demand for material handling equipment across supply chains.

3. Road Construction Equipment

Road construction equipment represents one of the most infrastructure-dependent segments within the construction equipment market in Africa. Asphalt pavers, motor graders, rollers, and compactors form the core machinery used in building and maintaining transport networks.

Governments across Africa prioritise road infrastructure to improve connectivity, reduce logistics costs, and support economic growth. This creates sustained equipment demand in Africa’s construction sector, particularly for highway and rural road projects.

Key technical considerations in this segment include:

- Compaction efficiency measured by the density and uniformity of road surfaces.

- Paving accuracy, which determines road durability and maintenance cycles.

- Equipment productivity defined by output per hour in large-scale projects.

Motor graders play a critical role in road alignment and surface preparation, while asphalt pavers ensure consistent material placement. Compactors, including vibratory rollers, deliver the final structural integrity of road layers.

The analysis of growth in the African construction machinery market indicates that this segment will experience steady expansion due to the following:

- Ongoing development of regional transport corridors.

- Increased funding for rural road connectivity.

- Expansion of urban road networks to support population growth.

This segment directly reflects government spending patterns, making it a reliable indicator of heavy equipment market growth in Africa.

4. Concrete Equipment

Concrete equipment supports the structural phase of construction, making it essential within the construction equipment market in Africa. This segment includes concrete mixers, batching plants, and pumping systems, all of which ensure consistent and efficient concrete production and placement.

Urbanisation and infrastructure developments drive demand in this segment. High-rise buildings, bridges, and industrial facilities require large volumes of concrete, increasing reliance on advanced equipment.

Batching plants represent the most critical component, as they control the quality and consistency of concrete. Modern plants integrate automated systems to do the following:

- Maintain precise material ratios.

- Monitor production output in real time.

- Reduce material waste and improve efficiency.

Concrete pumps, particularly boom pumps, enable placement in high-rise and large-scale projects, increasing speed and reducing labour requirements.

Technical factors influencing this segment include:

- Output capacity, measured in cubic metres per hour.

- Pumping range and height for vertical construction.

- Automation and digital control systems for quality assurance.

The construction equipment industry in Africa is seeing increased adoption of mobile batching plants, which offer flexibility for remote and infrastructural projects. As the future of the construction equipment market in Africa evolves, this segment will play a critical role in improving construction quality and efficiency across the continent.

Regional Analysis on Construction Equipment Across Africa

Regional dynamics define the structure and growth trajectory of the construction equipment market in Africa. Each region presents distinct demand drivers, project types, and investment patterns, shaping the overall growth analysis of the African construction machinery market.

1. East Africa – Infrastructure-Led Growth

East Africa leads infrastructure-driven expansion in the construction equipment market, supported by strong government investment in transport and energy projects. Countries, such as Kenya, Tanzania, and Ethiopia, continue to prioritise large-scale infrastructure development.

Key demand drivers include:

- Development of standard-gauge railway networks.

- Expansion of ports and logistics hubs.

- Investment in renewable and hydropower energy projects.

These projects require extensive deployment of earthmoving and road construction equipment, reinforcing the forecast for the construction equipment market in Africa from 2025 to 2035.

2. West Africa – Resource and Urban Expansion

West Africa combines resource-driven demand with rapid urbanisation to create a diversified construction machinery market. Nigeria and Ghana lead regional growth through oil, gas, and housing projects.

Urban expansion drives demand for:

- Concrete and material handling equipment.

- Mid-size earthmoving machinery for residential construction.

Simultaneously, oil and gas projects sustain demand for heavy-duty equipment, aligning with the forecast for heavy equipment demand in Africa 2035.

3. Southern Africa – Mining-Driven Demand

Southern Africa remains the most mature equipment market, driven by mining operations. South Africa and Zambia dominate this segment, with high utilisation rates for heavy machinery.

Mining operations require:

- High-capacity excavators and loaders.

- Rigid and articulated dump trucks.

- Continuous equipment operation under demanding conditions.

This region reflects the highest equipment intensity within the construction equipment market in Africa, reinforcing long-term demand stability.

4. North Africa – Industrial and Energy Investments

Northern Africa demonstrates a more industrialised growth pattern in the construction equipment market. Egypt and Morocco lead in manufacturing, energy, and large-scale infrastructure projects.

Key drivers include:

- Renewable energy investments, particularly solar and wind.

- Expansion of industrial manufacturing zones.

- Government-led mega infrastructure projects.

This region is seeing increasing adoption of advanced equipment and technology that aligns with global standards.

5. Central Africa – Emerging Equipment Markets

Central Africa represents an early-stage but high-potential segment within the construction equipment market in Africa. Infrastructure gaps create significant demand for basic construction equipment.

Key characteristics include the following:

- Limited but growing infrastructure investment.

- High dependency on imported equipment.

- Gradual expansion of contractor capacity.

The construction equipment market in Africa, forecast 2025 to 2035, identifies Central Africa as a long-term growth frontier as investment increases.

Africa Construction Machinery Market Growth Analysis

The Africa construction machinery market growth analysis highlights a structurally expanding market driven by regional differentiation, sectoral demand, and evolving supply chains. The construction equipment market in Africa does not follow a uniform trajectory. Instead, it reflects layered growth influenced by infrastructure pipelines, mining cycles, and access to financing.

East and West Africa drive volume growth through infrastructure and urban expansion, while Southern Africa maintains high-value demand through mining operations. North Africa contributes through industrial and energy investments, creating a diversified growth profile.

Key structural insights include:

- Regional growth divergence: East Africa leads in infrastructure, Southern Africa in mining, and North Africa in industrial development.

- Shift toward higher utilisation: Contractors prioritise equipment efficiency over fleet size expansion.

- Localisation trends: Increasing utilisation: contractors prioritise the adoption of CKD assemblies, which reduces import dependency and improves supply chain resilience.

The construction equipment market in Africa, forecast from 2025 to 2035, confirms that demand will increasingly align with project scale and financing availability rather than opportunistic procurement.

The heavy equipment market growth in Africa will therefore depend on three critical factors:

- Infrastructure investment consistency.

- Access to financing and leasing solutions.

- Expansion of after-sales and maintenance ecosystems.

These dynamics position the construction equipment market in Africa as one of the most strategically important growth segments in the global construction industry.

Construction Equipment Supply Chain and Distribution Landscape

The supply chain architecture defines accessibility, pricing, and operational efficiency within the construction equipment market in Africa. Unlike mature markets, Africa operates a multi-layered distribution system influenced by import dependence, dealer networks, and emerging localisation strategies.

Most equipment enters African markets through import channels, primarily from Asia and Europe. Chinese OEMs currently dominate volume shipments due to cost competitiveness, accounting for $4 billion in construction machinery exports to Africa in the first half of 2025 alone, a 51.6% year-on-year increase. The European and Japanese manufacturers maintain a presence in premium segments

The supply chain operates across three key layers:

- Primary importers and distributors: These entities handle bulk procurement and national-level distribution.

- Regional dealers: They provide equipment sales, financing support, and after-sales services.

- Local service providers: They handle maintenance, spare parts, and field-level support.

The expansion of dealer networks has improved accessibility within the construction equipment market in Africa, particularly in high-growth markets. However, distribution efficiency still varies significantly across regions.

A major structural shift involves the rise of local assembly. Countries such as Kenya and Nigeria increasingly attract CKD assembly operations such as the Sintrouk CFAO Mobility and Dangote Sinotruk, which:

- Reduce import duties and logistics costs.

- Improve equipment availability.

- Support local employment and industrialisation.

Spare parts and maintenance ecosystems remain critical constraints. Contractors often face downtime due to limited parts availability and weak service networks. As a result, OEMs and distributors now prioritise post-sales infrastructure as a competitive differentiator.

The construction equipment market in Africa increasingly rewards suppliers who integrate sales, financing, and lifecycle support into a single value proposition.

Further Reading: 22 Best Chinese Tipper Truck Dealers in Africa: Verified List of Trusted Suppliers

Technology and Innovation in Construction Equipment

Technology is reshaping the construction equipment market in Africa, moving the industry from labour-intensive operations to data-driven efficiency. Trends in the construction equipment industry in Africa show a gradual, yet decisive, shift toward digitalisation and automation.

Telematics systems now form the backbone of modern fleet management. These systems provide real-time insights into:

- Equipment utilisation rates.

- Fuel consumption patterns.

- Maintenance requirements and fault diagnostics.

Contractors who deploy telematics achieve measurable gains in operational efficiency. They reduce downtime, optimise fuel usage, and extend the equipment’s lifespan. This directly influences profitability within the construction machinery market in Africa.

Automation also continues to evolve. Advanced mining operations still limit fully autonomous equipment, but semi-autonomous features are becoming increasingly common. These include:

- Automated grading systems.

- Machine control for excavation accuracy.

- Operator-assist technologies that improve productivity.

Electrification represents a long-term trend within the future of the construction equipment market in Africa. Urban construction projects increasingly explore electric equipment to reduce emissions and operating costs, despite limited adoption due to infrastructure constraints.

Digital construction integration further enhances efficiency. Contractors now align equipment with Building Information Modelling (BIM) and project management systems, enabling the following:

- Precise project planning and execution.

- Reduced material waste.

- Improved coordination across project phases.

These innovations collectively define the next phase of the construction equipment market in Africa, forecast for 2025 to 2035, where efficiency and intelligence drive competitive advantage.

Investment Trends and Financing Landscape

Financing remains a decisive enabler within the construction equipment market in Africa, directly influencing equipment accessibility and fleet expansion. The growth of the heavy equipment market in Africa increasingly depends on structured financing solutions rather than outright capital purchases.

Contractors now adopt a mix of financing models, including:

- Equipment leasing for flexibility and lower upfront costs.

- Asset financing using equipment as collateral.

- Bank loans for large-scale fleet acquisitions.

This shift reflects a broader transformation in equipment demand in Africa’s construction sector, where liquidity management is as important as equipment ownership. Financial institutions, including regional banks and development finance institutions, continue to expand their role. The African Development Bank actively supports regional infrastructure financing, indirectly boosting equipment demand.

Leasing markets are also expanding rapidly. Contractors prefer leasing because it:

- Reduces upfront capital requirements.

- Provides flexibility for short-term projects.

- Transfers some maintenance responsibility to providers.

Ownership models still dominate in large firms, particularly those operating in mining and long-term infrastructure projects. However, SMEs increasingly rely on leasing and asset financing to participate in the construction equipment market in Africa. As the financing landscape continues to shape the heavy equipment demand forecast for Africa 2035, it is crucial to understand some of the financing strategies for construction equipment in Africa, particularly as access to capital improves.

Further Reading: Financing Construction Equipment in Africa: 7 Proven Options

Challenges Facing the Construction Equipment Market in Africa

The construction equipment market in Africa operates within a complex structural environment where capital intensity, regulatory fragmentation, and macroeconomic volatility directly influence market performance. These constraints do not slow growth uniformly. They reshape procurement strategies, influence decisions about equipment lifecycles, and determine the pace of heavy equipment market growth in Africa.

The construction equipment market in Africa, forecast for 2025 to 2035, indicates that overcoming these constraints will require coordinated improvements to financing systems, supply chains, and policy frameworks. Contractors, OEMs, and financiers must align their strategies with these realities to sustain growth in equipment demand in Africa’s construction sector.

1. High Capital Costs

High capital intensity remains the most immediate barrier within the construction equipment market in Africa. Contractors must make a significant upfront investment to acquire equipment, particularly high-capacity machinery used in infrastructure and mining projects.

Equipment pricing reflects multiple cost layers. Manufacturers price machinery in foreign currencies, primarily US dollars or euros. Import duties, logistics costs, and distributor margins further increase acquisition costs across African markets. As a result, contractors often face pricing levels that exceed those in more mature markets, even after adjusting for purchasing power.

Financing constraints amplify this challenge. Many contractors operate in environments where:

- Local interest rates remain elevated due to macroeconomic risk profiles.

- Lending institutions apply strict collateral requirements.

- Loan tenures remain shorter than the equipment lifecycle.

These conditions limit participation, particularly for SMEs, and slow the expansion of the construction machinery market in Africa. From a technical perspective, contractors increasingly evaluate the total cost of ownership rather than just the upfront price. This includes:

- Fuel consumption over the equipment lifecycle.

- Maintenance and spare parts costs.

- Residual value at the end of operational use.

This shift reflects broader trends in the construction equipment industry in Africa, where capital efficiency and lifecycle performance determine procurement decisions.

2. Maintenance and After-Sales Gaps

Maintenance infrastructure represents a critical constraint within the construction equipment market in Africa. Equipment performance depends heavily on consistent servicing, timely availability of spare parts, and access to skilled technicians. However, many markets lack the ecosystem necessary to support high equipment utilisation.

Contractors frequently encounter operational inefficiencies due to:

- Delays in sourcing spare parts, particularly for imported machinery.

- Limited availability of trained service technicians.

- Inadequate diagnostic tools for modern, technology-enabled equipment.

These gaps increase downtime, reduce equipment productivity, and raise operational expenses. In high-intensity sectors such as mining, even short periods of downtime can significantly impact output and revenue.

OEMs and distributors increasingly recognise after-sales service as a competitive differentiator in the construction equipment market in Africa. Leading players now invest in:

- Regional parts distribution hubs to reduce delivery times.

- Training programmes to develop local technical expertise.

- Integrated service contracts that bundle maintenance with equipment sales.

The analysis of growth in the African construction machinery market confirms that markets with stronger after-sales ecosystems achieve higher equipment utilisation rates and faster fleet expansion. This makes maintenance infrastructure a critical factor in sustaining the growth of the heavy equipment market in Africa.

3. Regulatory and Import Constraints

Regulatory fragmentation continues to shape the construction equipment market in Africa, creating complexity for both suppliers and contractors. Each country maintains distinct import regulations, tax structures, and compliance requirements, which complicate cross-border equipment movement.

Import duties and taxes significantly affect equipment pricing. In some markets, cumulative duties, value-added tax, and port handling charges can increase equipment costs by a substantial margin. This situation directly impacts affordability and slows adoption within the construction machinery market in Africa.

Procurement timelines also face delays due to:

- Lengthy customs clearance processes.

- Documentation requirements for compliance certification.

- Inconsistent enforcement of regulatory standards across regions.

These inefficiencies increase project risk and disrupt equipment deployment schedules, particularly in time-sensitive infrastructure projects.

However, regulatory environments are gradually evolving. Regional initiatives, such as the African Continental Free Trade Area, aim to harmonise trade policies and reduce barriers. Over time, these changes will improve equipment mobility and support the construction equipment market in Africa from 2025 to 2035.

Until then, contractors must integrate regulatory risk into procurement strategies, factoring in lead times, cost variability, and compliance requirements.

4. Currency and Economic Volatility

One of the biggest macroeconomic risks in the African construction equipment market is currency volatility. Since most equipment transactions occur in foreign currencies, fluctuations in exchange rates directly affect procurement costs and financial planning.

Depreciation of local currencies increases the cost of imported equipment, forcing contractors to either delay purchases or absorb higher costs. This volatility introduces uncertainty into project budgeting, particularly for long-term infrastructure contracts.

Key impacts include:

- Increased capital expenditure during periods of currency depreciation.

- Reduced predictability in equipment pricing.

- Higher financing costs due to risk premiums applied by lenders.

Economic instability further compounds these challenges. Inflationary pressures increase operating costs, while fiscal constraints may delay government infrastructure spending. These factors influence both supply and demand within the construction equipment market in Africa.

This heavy equipment demand forecast for Africa 2035 accounts for these risks, emphasising the necessity of financial resilience and adaptive procurement strategies. Contractors are increasingly adopting hedging mechanisms, diversifying funding sources, and prioritising flexible financing models to mitigate currency exposure.

Competitive Landscape and Key Market Players

The construction equipment market in Africa features a multi-layered competitive landscape, with global OEMs, regional distributors, and Chinese manufacturers competing across distinct market segments. Each group leverages specific strengths to capture market share within the evolving construction machinery market in Africa.

Caterpillar and Komatsu are two of the biggest global manufacturers in the high-end market. These companies position their products based on durability, advanced technology, and lifecycle efficiency. Their equipment typically commands higher upfront costs but delivers lower operating expenses over time.

In contrast, Chinese manufacturers such as SANY and XCMG have rapidly expanded their presence, particularly in volume-driven segments of the construction equipment market in Africa. Their competitive advantage rests on three core factors:

- Lower acquisition costs, enabling broader market penetration.

- Flexible financing arrangements, often supported by export credit facilities.

- Extensive distribution networks across emerging markets.

Regional distributors play a critical intermediary role in equipment sales and maintenance. They provide market access, localised support, and after-sales services, bridging the gap between OEMs and contractors. We did a market analysis of the trusted Chinese tipper truck dealers in Africa.

Strategic partnerships increasingly define competitive positioning. OEMs collaborate with local firms to establish assembly plants, expand dealer networks, and improve service delivery. These partnerships reduce costs, improve responsiveness, and strengthen market presence.

The construction equipment market in Africa, forecast 2025 to 2035, suggests that competition will intensify, with success depending on the ability to integrate:

- Cost competitiveness.

- Financing accessibility.

- Lifecycle support and service reliability.

Construction Equipment Demand Forecast Africa 2035

The heavy equipment demand forecast for Africa 2035 reflects a structurally expanding market driven by long-term economic and demographic factors. The forecast on the construction equipment market in Africa indicates that demand will increasingly align with infrastructure pipelines, resource extraction, and urban development.

Infrastructure remains the dominant demand driver. Governments continue to invest in transport networks, energy systems, and logistics infrastructure to support economic growth. These projects require large volumes of earthmoving and road construction equipment, which sustains the construction equipment market in Africa.

Mining represents the second major demand pillar. The global transition toward renewable energy increases demand for critical minerals such as copper and lithium. African countries with significant mineral reserves will experience sustained equipment utilisation in their extraction and processing operations.

Urban development forms the third pillar. Rapid population growth drives demand for housing, commercial buildings, and municipal infrastructure. Such growth increases demand for concrete and material handling equipment, reinforcing equipment demand in Africa’s construction.

The construction equipment market in Africa, forecast 2025 to 2035, shows a shift toward higher equipment intensity per project. Contractors increasingly rely on machinery to improve efficiency, reduce labour dependence, and meet project timelines. This trend confirms that the construction equipment market in Africa will continue to expand as a function of productivity requirements rather than simple project volume.

Strategic Opportunities for Contractors and Investors

The construction equipment market in Africa offers significant opportunities for stakeholders who adopt structured, data-driven strategies. Growth will not reward opportunistic investment. It will reward disciplined capital allocation aligned with African construction industry trends.

Contractors can unlock value by focusing on equipment segments with high utilisation rates, particularly earthmoving and road construction machinery. These segments deliver consistent demand across infrastructure and mining projects.

Leasing and rental markets provide another strategic lever. Contractors can reduce capital exposure while maintaining operational flexibility. This approach aligns with evolving trends in the construction equipment industry in Africa, where access increasingly replaces ownership.

Regional expansion also presents opportunities. High-growth markets in Eastern and West Africa offer strong demand potential due to infrastructure pipelines and urbanisation trends.

Risk management remains essential. Contractors and investors must address the following:

- Currency exposure through diversified financing structures.

- Operational risks through maintenance and service planning.

- Regulatory risks through compliance and market intelligence.

Those who integrate these strategies will outperform competitors in the evolving construction machinery market in Africa.

Future of the Construction Equipment Market in Africa

Digital transformation, sustainability, and localisation will determine the future of the construction equipment market in Africa. The convergence of these forces will reshape the procurement, deployment, and management of equipment across the continent.

Digital technologies will play a central role. Telematics, data analytics, and fleet management systems will enable contractors to maximise usage, reduce downtime, and improve cost efficiency. This marks a shift toward performance-driven operations within the construction equipment market in Africa.

Sustainability will become increasingly important. Governments and international institutions will push for cleaner construction practices, encouraging the adoption of fuel-efficient and low-emission equipment. While electrification remains in early stages, urban projects will lead adoption due to regulatory and environmental pressures.

Localisation will strengthen supply chains. Expansion of local assembly and manufacturing will reduce dependency on imports, improve equipment availability, and support economic development. This is in line with long-term predictions for the construction equipment market in Africa from 2025 to 2035.

These trends collectively define the future of the construction equipment market in Africa, positioning the continent as a key driver of global construction equipment demand.

Conclusion: Strategic Direction of the Construction Equipment Market in Africa

The construction equipment market in Africa will continue to expand as infrastructure pipelines mature, mining investments accelerate, and urbanisation intensifies across key regions. The construction equipment market in Africa, forecast 2025 to 2035, confirms that demand will shift from fragmented procurement toward structured, capital-driven growth, positioning Africa as a central pillar in global equipment demand. Stakeholders who align with African construction industry trends understand the heaviness. The next phase of market leadership will be defined by the equipment demand forecast for Africa 2035 and the response to evolving equipment demand in Africa’s construction.

Looking ahead, capital allocation will increasingly prioritise efficiency, lifecycle performance, and financing innovations. Contractors and investors who leverage insights from the growth analysis of the construction machinery market in Africa, integrate digital capabilities, and anticipate the future of the construction equipment market will secure a long-term competitive advantage. The market will reward those who treat equipment not as a cost center but as a strategic asset that drives productivity, scalability, and sustainable value creation.

Build Smarter Equipment Strategies With Us

Stay ahead in the construction equipment market in Africa with clear insights on demand, financing, and market trends. Explore more analysis and make smarter investment decisions with Construction Frontier.