Africa’s Airport Mega-Projects: Definitive Guide to the Continent’s Promising USD30bn+ Aviation Future

Africa’s airport mega-projects have entered their busiest construction cycle in the continent’s history, with more than USD 30 billion committed across Rwanda, Kenya, Ethiopia, Egypt, Nigeria, and Angola alone. Rwanda’s Bugesera International Airport, Ethiopia’s USD 12.5 billion Bishoftu International Airport, Kenya’s re-tendered Jomo Kenyatta International Airport upgrade, and Egypt’s USD 3.5 billion Cairo Terminal 4 are each racing to capture a market that the International Air Transport Association expects to grow by 6% in 2026, the fastest of any region on earth. This guide breaks down every major African airport mega-project reshaping the continent’s connectivity, the engineering choices behind them, and what they mean for investors, contractors, and policymakers tracking African aviation infrastructure over the rest of the decade.

Technical Snapshot: Africa’s Airport Mega-projects Core Project Specifications

| Project | Specification |

| Total continental pipeline value | Over USD 30 billion in active or committed airport construction |

| Largest single project | Bishoftu International Airport, Ethiopia: USD 12.5 billion |

| Largest planned capacity | Bishoftu, up to 110 million passengers annually at full build-out |

| Fastest-growing aviation market globally | Africa, forecast at 6.0% passenger growth in 2026 (IATA) |

| Busiest hub under active renovation | Jomo Kenyatta International Airport, Nairobi (9 million passengers, rebuilding toward 22 million) |

| Newest fully operational mega-hub | Dr. António Agostinho Neto International Airport, Angola (USD 3.8 billion, 15 million passenger capacity) |

| Cargo-first design leader | Bishoftu International Airport, engineered for 3.73 million tonnes of freight annually |

Africa’s airport mega projects are no longer isolated national vanity projects. They form a competing network of hubs, each fighting for the same transcontinental transfer traffic that has bypassed the continent for decades, and each reshapes the business case for Africa’s airport mega-projects across the wider region.

Introduction: Africa’s Airport Mega Project Boom

Africa’s airport mega projects have moved from paper to concrete faster in the past eighteen months than in the previous decade combined. Rwanda has poured billions into Bugesera. Ethiopia has broken ground on what may become the busiest airport ever built. Kenya has torn up one contract and signed another for its main gateway. Egypt has approved a fourth terminal at Cairo. Nigeria is stripping its flagship international terminal to the concrete frame. None of these decisions happened in isolation. They form part of a broader continental push, detailed in Construction Frontier’s complete guide to Africa’s transport infrastructure revolution, in which more than 20 transport mega-projects are converging to close Africa’s connectivity gap.

The scale of the opportunity explains the urgency behind every African airport mega-project profiled in this guide. Africa carries less than a quarter of its share of global air traffic despite housing 18% of the world’s people, and only 19% of intra-African routes offer direct flights. Every government covered here is betting that whoever builds the biggest, fastest, cheapest-to-operate terminal first captures the connecting traffic now routing through Dubai, Istanbul, or Paris. That strategic insight is what makes Africa’s new airports in 2026 worth tracking, whether the reader is an engineer scoping a tender, an investor assessing risk, or a policymaker weighing the debt implications of a multi-billion-dollar runway.

This guide covers the full list of African airport mega-projects currently under construction or in advanced planning: Rwanda’s Bugesera International Airport, Kenya’s Jomo Kenyatta International Airport overhaul, Ethiopia’s Bole International Airport and its successor Bishoftu International Airport, Egypt’s Cairo International Airport Terminal 4, Nigeria’s Murtala Muhammed rebuild, Angola’s Dr. António Agostinho Neto International Airport, and a growing tail of secondary upgrades from Cape Town to Sharm El Sheikh. Each entry includes verified costs, capacity targets, contractors, and financing structures so that anyone assessing African airport mega-projects for investment, procurement, or reporting purposes has a single, continuously updated reference point.

The Investment Case Behind Africa’s Airport Mega Projects

Understanding why so much capital has converged on African aviation infrastructure in such a short window requires looking beyond any single terminal to the demand curve driving every decision in this section. Three factors, growth rate, connectivity failure, and capital appetite, explain why Africa’s airport mega-projects have accelerated simultaneously rather than one at a time.

The Investment Case Behind Africa’s Airport Mega Projects

Understanding why so much capital has converged on African aviation infrastructure in such a short window requires looking beyond any single terminal to the demand curve driving every decision in this section. Three factors, growth rate, connectivity failure, and capital appetite, explain why Africa’s airport mega-projects have accelerated simultaneously rather than one at a time.

Passenger Demand Is Outpacing Every Other Region

IATA’s 2026 industry outlook puts African passenger growth at 6.0%, ahead of the global average of 4.9% and the fastest among the regions tracked. African carriers posted an 11.7% year-on-year demand increase to start 2026, more than double the global figure, while cargo volumes climbed 21% in February alone, the strongest of any region worldwide.

Over the next two decades, the market is projected to grow at roughly 4.1% annually, reaching more than 400 million passengers by the mid-2040s, with East Africa expected to lead the expansion. That trajectory alone justifies the wave of African airport expansion projects now under construction, because none of the continent’s existing gateways, Nairobi, Addis Ababa, Lagos, or Cairo, were designed for the volumes they are already carrying, let alone the volumes forecast for the next twenty years.

Set against Construction Frontier’s guide to the world’s ten biggest airport megaprojects, several of the African projects profiled here, particularly Bishoftu, already rank among the largest airport builds anywhere on the planet by both cost and planned capacity. Aviation already supports an estimated 8.1 million jobs across the continent and roughly USD 75 billion in GDP, figures that every finance ministry weighing a new terminal against competing budget priorities now cites directly.

The Cost of Fragmented Skies

Africa’s aviation infrastructure development problem has never really been a shortage of demand. There has been a shortage of direct routes, open skies, and affordable operating costs. Only 19% of intra-African city pairs have a direct connection, forcing passengers and cargo through European or Gulf hubs even for journeys within the same continent.

Fuel costs in Africa run roughly 17% above the global average, and airport charges and taxes are 12 to 15% higher, a combination that leaves African carriers earning barely USD 1.30 in net profit per passenger, compared with a global average of USD 7.90. The Single African Air Transport Market, now backed by 38 signatories representing over 80% of intra-African traffic, is slowly dismantling the bilateral restrictions behind this dysfunction, and every new terminal covered in this guide is being built with SAATM liberalisation, not the status quo, in mind.

Blocked airline funds remain a related drag: Africa accounts for roughly 79% of all globally blocked airline revenue, a distortion that shapes route economics as much as any runway shortage does.

Capital Is Following the Growth Story

Qatar Airways holds a 60% stake in Bugesera International Airport. Ethiopian Airlines is self-funding 30% of the Bishoftu project, with the African Development Bank and the US International Development Finance Corporation covering the remainder. China Communications Construction Company has taken on Kenya’s re-tendered JKIA contract, following the same state-backed contractor model that built Angola’s Agostinho Neto airport and much of Ethiopia’s rail and energy infrastructure.

Egypt is self-financing Cairo’s Terminal 4 through its Holding Company for Airports and Air Navigation rather than opening the airport itself to foreign ownership. Nigeria has gone down the same route domestically, funding the Murtala Muhammed rebuild through its federal budget and awarding the contract to a Chinese state contractor rather than to a foreign concession. Each financing structure reflects a different appetite for sovereign risk, and each is a case study in how African governments are learning to structure mega-airport projects after the collapse of Kenya’s original Adani concession exposed the political cost of opaque, single-partner deals.

African Countries Building New Airports: A Continental Overview

African airport mega-projects are not confined to a single region or funding model. The table below summarises the biggest airport projects in Africa currently under construction, recently completed, or in advanced procurement, giving a single reference point for the list of African airport mega projects covered throughout this guide.

Table 1: African Countries Building New Airports

| Country | Project | Status |

| Rwanda | Bugesera International Airport | Under construction, targeting 2027-2028 |

| Kenya | Jomo Kenyatta International Airport upgrade | Re-tendered after Adani collapse, construction beginning in 2026 |

| Ethiopia | Bishoftu International Airport | Broke ground in January 2026; Phase 1 targeted for 2030 |

| Ethiopia | Bole International Airport | Operational, Phase 3 expansion completed late 2025 |

| Egypt | Cairo International Airport Terminal 4 | Approved; construction expected to take four years |

| Nigeria | Murtala Muhammed International Airport Terminal 1 | Under a 22-month structural rebuild since March 2026 |

| Angola | Dr. António Agostinho Neto International Airport | Operational since 2023-2025, phased opening |

| South Africa | Cape Town International Airport | Major works, including a new runway, beginning 2026 |

This snapshot of new airports under construction in Africa is not exhaustive. Smaller upgrades are advancing in parallel across Ghana, Senegal, Tanzania and Morocco, but the eight programmes above account for the overwhelming majority of committed capital in Africa’s current aviation infrastructure development cycle, and each is examined in detail in the sections that follow.

East Africa’s Race for Aviation Supremacy

East Africa has become the most competitive theatre for African aviation hubs, with three governments simultaneously building or rebuilding gateways designed to capture the same transcontinental transfer traffic. Rwanda, Kenya and Ethiopia are not coordinating; they are racing, and the projects below show three very different approaches to winning that race and three different templates for African airport construction more broadly.

Rwanda’s Bugesera International Airport: A Qatari-Backed Gateway

Rwanda began clearing land for Bugesera International Airport in 2017, and construction has since undergone several redesigns, a change of lead contractor, and a completion date that has slipped from 2019 to a firm target of 2027 or 2028. Qatar Airways holds a 60% equity stake, with the Rwandan government retaining 40%, and the airline’s involvement has shaped the project’s ambitions: a 3,750-metre runway capable of handling an Airbus A380 or Boeing 747-8, a 130,000-square-metre terminal designed for 7 to 8 million passengers in its first phase, and a dedicated cargo terminal built for 150,000 tonnes annually.

The government secured improved World Bank-backed concessional financing in February 2026, reducing the interest burden on the roughly USD 2 billion project and replacing nearly USD 400 million in commercial borrowing with lower-cost, drawdown-based funding. Phase two, targeted for 2032, would double capacity to 14 million passengers a year, positioning Kigali as a direct rival to Nairobi and Addis Ababa for East African transfer traffic. Engineering consultancy Zutari has led design review and construction supervision throughout, using photogrammetry and virtual-reality modelling to keep the fast-tracked build on schedule despite its long history of delay.

Further Reading: Bugesera Airport: 5 Definitive Engineering Insights Behind Rwanda’s Promising USD2bn Aviation Hub

Kenya’s Jomo Kenyatta International Airport: Rebuilding After the Adani Collapse

No single episode illustrates the political risk embedded in Africa’s airport mega projects better than the saga surrounding Kenya’s new airport plan. India’s Adani Group signed a privately initiated proposal in March 2024 to rebuild and operate JKIA under a 30-year concession valued at roughly USD 1.85 billion. Legal challenges, transparency concerns and, ultimately, US bribery and fraud indictments against the group’s founder led President William Ruto to cancel the deal in November 2024, with the Kenya Airports Authority confirming formal termination of the roughly Ksh 238 billion agreement in February 2026.

Kenya then re-tendered the project, and China Communications Construction Company was awarded a contract worth roughly Ksh 375 billion (about USD 2.9 billion) through the National Infrastructure Fund, structured across two phases: an 18-month upgrade lifting capacity to 12 million passengers, followed by a second phase adding a new 4,500-metre parallel runway and a 230,000 square metre X-shaped terminal built for an additional 10 million passengers.

JKIA currently handles roughly 9 million passengers against a design capacity of 7.5 million, and officials expect demand to reach 22 million by the mid-2040s, with cargo volumes projected to more than double from 407,000 tonnes to 860,000 tonnes by 2045. The switch from an Indian operator-led concession to a Chinese contractor-led public financing model marks one of the clearest before-and-after case studies in how African governments are rethinking airport procurement after a failed deal, and it remains one of the most closely watched examples of African airport construction anywhere on the continent.

Ethiopia’s Twin Bet: Bole International Airport and Bishoftu International Airport

Ethiopia is running two airport strategies at once, and both matter to anyone studying African airport mega-projects. Bole International Airport remains Ethiopian Airlines’ operational hub today, handling more than 22 million passengers a year after the completion of Phase 3 in late 2025, including a USD 50 million renovation of the domestic terminal that doubled its footprint to 25,750 square metres and its baggage-handling capacity.

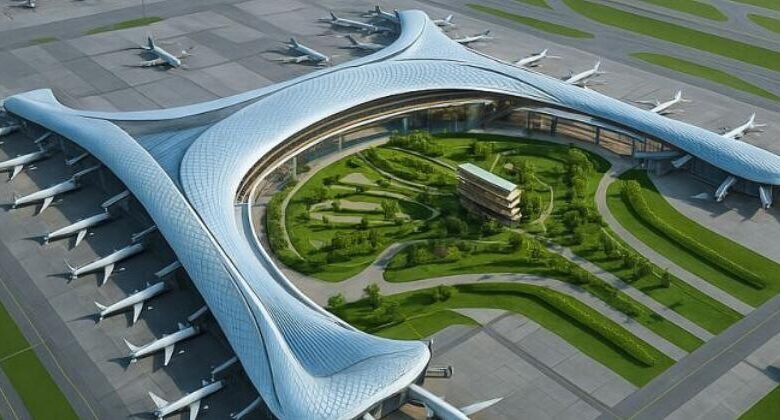

But Bole sits close to its structural ceiling, with capacity near 25 million passengers and little room left to expand, which is why the government broke ground in January 2026 on Bishoftu International Airport, a USD 12.5 billion project 40 kilometres outside the capital, designed by Zaha Hadid Architects. Bishoftu’s first phase, targeted for 2030, delivers two runways and an annual capacity of 60 million passengers; the full build-out reaches 110 million passengers, four runways, and 270 aircraft stands, a scale that would rank it among the busiest airports on earth and comfortably the largest of any African aviation hub.

Ethiopian Airlines is contributing 30% of the project cost from its own balance sheet, with the African Development Bank committing USD 500 million and the US International Development Finance Corporation providing additional support. Roughly 80% of Bishoftu’s expected traffic will be pure transfer passengers, and its 660,000-square-metre X-shaped terminal is engineered to minimise walking distances across four piers, a direct response to competition from Gulf hub designs.

The site itself sits nearly 400 metres lower in elevation than Bole, letting fully loaded aircraft take off in thicker air with less fuel burn on longer non-stop routes, a detail that speaks to how seriously the engineering team treated performance economics rather than architectural spectacle alone.

Table 2: East Africa’s Competing Airport Mega Projects

| Airport | Country | Investment | Target Capacity |

| Bugesera International Airport | Rwanda | ~USD 2 billion | 7-8 million (Phase 1), 14 million (Phase 2, 2032) |

| Jomo Kenyatta International Airport | Kenya | ~USD 2.9 billion | 12 million (Phase 1), 22 million (Phase 2) |

| Bishoftu International Airport | Ethiopia | USD 12.5 billion | 60 million (Phase 1, 2030), 110 million (full build) |

| Bole International Airport | Ethiopia | USD 50 million (recent domestic terminal upgrade) | ~25 million (near capacity) |

North Africa’s Terminal Wars: Cairo’s USD 3.5 Billion Reset

North Africa’s biggest airport story in 2026 belongs to Egypt, where aviation minister Sameh El-Hefny has confirmed plans for a fourth terminal at Cairo International Airport after years of the facility running past its original design limits. Terminal 4 is estimated to cost between USD 3.5 billion and USD 4.5 billion, depending on the final design scope, and will be funded through a self-financing partnership between Egypt’s Holding Company for Airports and Air Navigation and other national entities, rather than foreign concession capital.

The new terminal alone is expected to handle 30 to 40 million passengers a year, lifting Cairo’s total capacity from roughly 28 million today to as much as 60 to 65 million once complete, alongside a new cargo city with an initial 1 million tonne capacity, expandable to 2 million tonnes. Construction is projected to take approximately four years once it is fully underway, with the visual identities of Terminals 2, 3 and 4 unified into a single modern presentation.

Egypt has explicitly ruled out privatising ownership of the airport itself, with El-Hefny stating publicly that Egyptian airports “will remain a sovereign asset of the state”, though the government is opening management and commercial operations at smaller gateways, including Hurghada, to private-sector partners through International Finance Corporation-backed feasibility work covering eleven airports nationwide. Sharm El Sheikh International Airport is also undergoing a parallel USD 420 million phased upgrade designed to lift capacity beyond 10 million passengers annually, and Hurghada International Airport recorded 10.5 million passengers in the 2024/2025 fiscal year, a 22% year-on-year increase that underscores why Egypt’s aviation infrastructure development strategy extends well beyond its capital.

Taken together, Cairo’s Terminal 4 and its supporting programme across secondary airports represent one of the most capital-intensive African airport expansion projects currently underway on the continent, built entirely on domestic financing rather than the airline-equity or foreign-contractor models seen further south.

West and Southern Africa’s Emerging Mega Hubs

While East Africa fights over transfer traffic and Egypt doubles down on Cairo, West and Southern Africa are running their own version of the same contest, driven less by transcontinental ambition and more by the sheer strain of ageing infrastructure against rising demand. These projects round out the fuller list of African airport mega projects that any continental overview needs to account for.

Nigeria’s Murtala Muhammed Rebuild

Nigeria’s Federal Executive Council approved ₦712 billion (approximately USD 500 million) for a full structural rebuild of Terminal 1 at Murtala Muhammed International Airport in Lagos, with the contract awarded to China Civil Engineering Construction Corporation. The terminal, originally designed in the 1970s for under a million passengers a year, was processing more than 8 million by 2024, and the government opted to strip the nearly 50-year-old building to its concrete frame rather than patch it further.

The 22-month project, which closed the terminal in March 2026, includes a new skywalk linking Terminal 1 to the newer Terminal 2, an enlarged apron for wide-body aircraft, and modernised mechanical, electrical, and security systems, as well as an 8,000-square-metre temporary departure hall that kept international carriers operating throughout construction. Once complete, the combined terminal complex is expected to handle 17.6 million passengers annually, positioning Lagos to defend its status as West Africa’s busiest gateway against Accra and Abidjan and giving Nigeria its own answer to the wider trend of African airport construction sweeping the continent.

Angola’s Agostinho Neto: A New Gateway to Southern Africa

Angola has already delivered one of the continent’s most complete airport mega-projects. The USD 3.8 billion Dr. António Agostinho Neto International Airport opened 40 kilometres southeast of Luanda after nearly two decades of delays, contract disputes and a construction restart, built by a Chinese state contractor and now handed to a consortium led by Corporación América Airports in partnership with Mota-Engil under a 20-year management concession. The facility’s two parallel runways, one stretching 4,200 metres, can accommodate an Airbus A380, and its first-phase terminal is built for 15 million passengers alongside a 130,000-tonne cargo terminal, expandable to 440,000 tonnes.

National carrier TAAG Angola Airlines completed its shift of international operations to the new airport in 2025, replacing the ageing Quatro de Fevereiro Airport entirely for commercial traffic and giving Southern Africa a genuine new long-haul gateway for the first time in a generation. Angola’s experience, spanning a 2005 launch, a 2017 contract termination and a 2020 restart before finally opening, is a useful cautionary benchmark for anyone assessing how long Africa’s new airports can realistically take to reach full operational maturity once construction resumes.

Cape Town and the Continent’s Long Tail of Expansion

Beyond the headline mega projects, a long tail of smaller but still significant upgrades is underway across the continent. Cape Town International Airport is set for major works beginning in 2026, including a new runway and expanded domestic and international terminals, part of South Africa’s broader push to protect Cape Town and Johannesburg’s role as Southern Africa’s logistics anchor. These projects rarely carry the multi-billion-dollar price tags of Bishoftu or Cairo, but collectively they represent a significant share of the list of African airport mega projects that industry trackers now monitor, and they matter just as much to the continent’s overall aviation infrastructure development trajectory as the flagship builds profiled elsewhere in this guide.

Taken together, the biggest airport projects in Africa now span every major sub-region: East Africa’s transfer-traffic contest, North Africa’s terminal-doubling strategy at Cairo, West Africa’s rebuild of ageing 1970s infrastructure in Lagos, and Southern Africa’s newly opened long-haul gateway in Luanda alongside Cape Town’s runway and terminal upgrades. No other infrastructure category on the continent currently attracts this breadth of simultaneous, high-value construction activity, which is precisely why African airport mega projects have become such a closely tracked segment of African aviation infrastructure spending for engineers, contractors and investors alike.

Further Reading: Bishoftu International Airport: Inside Ethiopia’s New Promising $12.5bn Mega Aviation Hub

The Outlook for Africa’s Airport Infrastructure Development Through 2030

Every project profiled above points toward the same conclusion: African airport infrastructure development has shifted from a series of one-off national builds into a coordinated, if uncoordinated, race between rival African aviation hubs. The next five years will decide which of these gateways actually convert construction spend into transfer traffic and which end up as an oversized terminal serving a market that never quite arrived.

Three trends will define this next phase of Africa’s airport infrastructure development. First, cargo will matter as much as passengers. Bishoftu, Bugesera and Cairo’s new cargo city are all being sized for freight volumes that did not exist a decade ago, betting that the African Continental Free Trade Area will finally give African aviation hubs a reason to move goods by air within the continent rather than routing them through Europe. Second, financing discipline will separate winners from laggards. Rwanda’s renegotiated, World Bank-backed terms on Bugesera show how much a government can save by fixing a financing structure mid-project, while Kenya’s Adani experience shows how much a poorly structured concession can cost in delay and reputational damage.

Governments still weighing investment decisions in Africa’s aviation hub in 2026 are watching both examples closely. Third, competition between African aviation hubs will intensify rather than settle. Kigali, Nairobi and Addis Ababa are all building toward the same transcontinental transfer passenger, and only one, perhaps two, of them will realistically capture the scale of traffic needed to justify their investment at full build-out.

For contractors, financiers and policymakers, the practical takeaway is straightforward: African countries building new airports today are not simply replacing tired 1970s-era terminals; they are competing for a specific, finite pool of intercontinental transfer traffic that Gulf carriers have controlled for a generation. The African aviation hubs that win this contest will be the ones that pair genuine engineering discipline, A380-capable runways, cargo-first terminal design and realistic financing structures, with the airline partnerships needed to actually fill the gates they are building. Africa’s airport mega-projects will continue to multiply through 2030, but only a handful will emerge as the continent’s true long-haul gateways.

Engineering and Financing Patterns Behind Africa’s Airport Mega Projects

Reading across all projects profiled in this guide reveals recurring engineering and financing choices that any contractor, lender, or policymaker entering this market needs to understand before committing capital to the next wave of African airport mega-projects.

1. Financing Structures: PPPs, Sovereign Debt and the Contractor-Led Model

Three financing models dominate this African aviation hub investment cycle. The first is the airline-anchored concession, seen in Bugesera, where Qatar Airways’ equity stake ties the airport’s fortunes directly to its own route network. The second is the contractor-led, state-financed model used in Angola, Kenya’s revised JKIA contract and Nigeria’s MMIA rebuild, where a state-owned Chinese construction firm delivers the asset against sovereign or development-bank financing rather than taking an operating stake. The third is full self-financing, Egypt’s approach at Cairo, where the state retains outright ownership and opens only management and commercial functions to private partners.

Kenya’s experience with Adani demonstrates the political fragility of a fourth model, the long-term foreign concession, when transparency and public participation are weak; the deal’s collapse after opposition from labour unions, civil society and, ultimately, US fraud indictments against the group’s founder forced a full restart of the procurement process and reshaped how the government now structures Africa airport expansion projects going forward.

2. Design Standards: Runways, Terminals and Cargo-First Engineering

Every mega-project in this guide has been engineered around two runways or more, A380-capable pavement strength, and a terminal footprint sized for connecting traffic rather than pure origin-and-destination demand. Bishoftu’s X-shaped, four-pier terminal and Cairo’s unified Terminal 2-3-4 concourse both prioritise minimising transfer walking distances, a direct response to competition from Gulf hub design.

Cargo capacity has become a parallel design driver in its own right: Bishoftu targets 3.73 million tonnes annually to support the African Continental Free Trade Area, while Bugesera, Angola’s Agostinho Neto and Cairo’s new cargo city each carry six-figure tonnage targets designed to capture e-commerce and perishable trade that previously moved through European hubs. This cargo-first approach is quickly becoming a defining feature of African airport construction, distinguishing the current generation of projects from the passenger-only terminals built across the continent a generation ago.

3. Risk Factors: Delays, Debt Sustainability and Political Exposure

Delay is the norm rather than the exception across this pipeline. Bugesera has slipped from an original 2019 completion date to 2027 or 2028, a near-decade-long delay that the IMF has flagged as a contributor to Rwanda’s public debt reaching an estimated 86.3% of GDP by 2026. Angola’s Agostinho Neto took nearly twenty years from initial planning to opening. Kenya lost roughly two years to the Adani cancellation and re-tender process alone.

For engineers and financiers assessing the next wave of African airport mega-projects, the pattern is consistent: technical execution risk is manageable, but financing structure and political transparency determine whether a project reaches completion on anything resembling its original timeline. Any credible African aviation hub investment thesis now has to price in this delay risk explicitly rather than treating published completion dates as fixed.

Further Reading: Cairo International Airport Expansion: 5 Remarkable Engineering Insights Driving Egypt’s $3.5bn Aviation Transformation

Conclusion: Africa’s Airport Mega Projects Are Rewriting the Continent’s Connectivity Map

Africa’s airport mega projects have stopped being isolated national infrastructure stories and have become a single continental contest for transfer traffic, cargo share and aviation-linked economic growth. Rwanda is betting on Qatari capital and speed to market, while Ethiopia is betting on scale, backing its own airline’s balance sheet against a USD 12.5 billion facility designed to out-build every Gulf hub in reach. Kenya is rebuilding trust in its procurement process after a costly political failure, while Egypt, Nigeria and Angola are proving that self-financed, state-led delivery can move just as fast as any foreign concession when the will exists.

The airports that open on schedule, control debt exposure and deliver genuine transfer efficiency will decide which African city becomes the next Dubai or Istanbul of the skies. The ones that stumble on financing or politics, as Kenya briefly did, will hand that advantage to a rival capital instead. The full list of African airport mega projects covered in this guide will keep growing through the rest of the decade, and the decisions being poured into concrete today, from Kigali to Bishoftu to Lagos, will determine how Africans, and the world, fly for the next fifty years. This pipeline of African airport mega projects will only accelerate as more African countries build new airports following this template.

Explore More of Africa’s Mega Projects

Africa’s airport expansion is part of a much larger infrastructure transformation. Explore Construction Frontier: Africa Mega Projects for expert technical analysis, engineering deep dives, and project reviews covering the continent’s most ambitious airports, railways, ports, highways, energy, and urban development megaprojects.